Last Updated: March 27, 2026

Advance Tax 2026

Who Pays, How to Calculate, 4 Due Dates and Section 424/425 Interest Guide

Part of the Income Tax India 2026: Income Tax India 2026 : A Complete Guide

Deepak is a freelance graphic designer earning Rs 15 lakh per year. He files ITR every July, pays whatever tax is due, and moves on. No advance tax. No quarterly payments.

His CA called him in April with a surprise: a Section 424 interest for not paying advance tax during the year. Plus Section 425 interest for the missed instalments. Total surprise bill: nearly Rs 6,600 — purely in interest, not tax.

Deepak’s mistake is extremely common among freelancers, self-employed professionals, investors with capital gains, and even salaried employees who have rental income or FD interest. Advance tax rules apply to anyone whose tax liability (after TDS) exceeds Rs 10,000 in a financial year — and missing the quarterly deadlines attracts automatic interest under Section 425 at 1% per month and Section 424 @ 1% per month from starting of next financial year till the month of payment.

This article covers everything: who must pay advance tax, the 4 due dates and percentages, how to calculate your liability, and how to pay.

| Rs 10,000 Tax liability threshold — above this advance tax is mandatory | 4 Dates June 15, Sep 15, Dec 15, Mar 15 — quarterly instalments | 1% / month Interest under Section 424 and 425 for default / deferment | Challan Official payment method — online via incometaxindia.gov.in |

1. Who Must Pay Advance Tax — and Who is Exempt

Advance tax is mandatory for any taxpayer whose estimated tax liability for the financial year exceeds Rs 10,000 after deducting TDS and TCS. It applies to individuals, HUFs, firms, companies, and all other taxpayers.

| Taxpayer Type | Advance Tax Required? | Reason |

| Salaried employee with only salary income (TDS deducted by employer) | Usually No | TDS covers the full tax liability. But if salary income + other income (rental, interest, capital gains) creates tax liability above Rs 10,000 after TDS — advance tax is required. |

| Freelancer or self-employed professional | Yes — if tax liability above Rs 10,000 | Assuming No TDS on freelance income, Full advance tax is to be paid in 4 instalments. |

| Investor with capital gains (LTCG/STCG) | Yes — if liability above Rs 10,000 | Capital gains realized during the year must be included in advance tax estimate. LTCG/STCG creates advance tax liability. |

| Business owner (non-presumptive) | Yes — 4 instalments | Standard 4-instalment schedule. Cannot defer to March 15 in one shot. |

| Presumptive taxation (Sec. 58) | Yes — but only 1 instalment | Entire advance tax in ONE instalment by March 15 only. |

| Senior citizen (resident, no business income) | EXEMPT | Resident senior citizens (60+ years) with no business/professional income are fully exempt from advance tax under Section 403. Section 424 and 425 interest also not applicable to them. |

2. Four Due Dates and Instalment Percentages

The advance tax for Tax Year 2026-27 must be paid in four instalments. The cumulative percentages and due dates are prescribed in the IT Act. These are CUMULATIVE percentages. Thus, by September 15, total advance tax paid must be at least 45% of full year liability, not just 45% of the instalment and so on.

| Instalment | Due Date | Cumulative % to Pay by This Date | Shortfall Threshold for 425 Interest | If Missed |

| 1st Instalment | June 15, 2026 | At least 15% of full year estimated tax | Interest if paid less than 12% by June 15 | Section 425 interest @ 1% p.m. on shortfall for 3 months |

| 2nd Instalment | September 15, 2026 | At least 45% cumulative of full year tax | Interest if cumulative less than 36% by Sep 15 | Section 425 interest @ 1% p.m. on shortfall for 3 months |

| 3rd Instalment | December 15, 2026 | At least 75% cumulative of full year tax | Interest if cumulative less than 75% by Dec 15 | Section 425 interest @ 1% p.m. on shortfall for 3 months |

| 4th Instalment | March 15, 2027 | 100% of full year advance tax | Interest if less than 100% by Mar 15 | Section 425 interest @ 1% p.m. on shortfall for 1 month. Section 424 interest starts from April 1. |

Special Rule for Presumptive Taxation (Section 58)

Taxpayers who have opted for presumptive taxation under Section 58 (business or professionals) need to pay only ONE instalment — 100% of advance tax by March 15 of the financial year. They can also pay by March 31. If even this single instalment is missed, Section 425 interest @ 1% for one month applies on the shortfall.

3. How to Calculate Your Advance Tax Liability

Advance tax is based on estimated income for the full year — not what you have earned so far. Here is the step-by-step calculation.

| Step | What To Do | Example (Freelancer, Tax Year 2026-27, New Regime) |

| Step 1: Estimate total income | Project your income from all sources for the full year: salary, freelance/business, rental, interest, capital gains. | Freelance income: Rs 14,00,000. FD interest: Rs 1,00,000. Total estimated income: Rs 15,00,000. |

| Step 2: Subtract deductions | Apply applicable deductions — 123, 126, 124, standard deduction (if applicable), HRA etc. | Standard deduction (if salaried): not applicable here. Taxable income: Rs 15,00,000. |

| Step 3: Calculate tax on taxable income | Apply new or old regime slab rates to taxable income. Add cess @4%. | New regime on Rs 15,00,000: Tax = Rs 1,05,000 + 4% cess = Rs 1,09,200. |

| Step 4: Subtract TDS already deducted | Check Form 26AS or AIS for TDS already deducted from your income by clients, banks etc. | TDS deducted by clients on freelance payments: Rs 18,000. Balance tax = Rs 1,09,200 minus Rs 18,000 = Rs 91,200. |

| Step 5: Check threshold | If balance tax liability (Step 4) exceeds Rs 10,000 — advance tax is mandatory. | Rs 91,200 > Rs 10,000 : advance tax mandatory. |

| Step 6: Split into 4 instalments | Apply the cumulative percentage schedule to determine each instalment. | Jun 15: 15% = Rs 13,680. Sep 15: 45% cumulative = Rs 41,040 . Dec 15: 75% cumulative = Rs 68,400. Mar 15: 100% cumulative = Rs 91,200. |

Important: advance tax is calculated on ESTIMATED income. If your actual income differs from estimate, you can adjust in later instalments. There is no penalty for revising upward, simply pay more in subsequent instalments. If you overestimate and overpay, the excess becomes a refund when you file ITR.

4. Section 424 and 425 : Interest Provisions Explained

These are two separate interest provisions that operate at different stages of the tax year. Many taxpayers confuse them.

| Feature | Section 424 | Section 425 |

| What triggers it | Total advance tax paid by March 31 is LESS than 90% of assessed tax | Any individual instalment shortfall during the year |

| When does it apply | After March 31 – starts from April 1 of assessment year | During the financial year – from the due date of each missed instalment |

| Interest rate | 1% per month or part of month | 1% per month or part of month |

| Calculated on | Assessed tax MINUS advance tax paid | Shortfall in each instalment (based on cumulative % schedule) |

| Period of interest | From April 1 of assessment year until tax is fully paid | 3 months for each of June, Sep, Dec instalments. 1 month for March instalment. |

| Can be avoided by | Paying at least 90% of full year tax before March 31 | Meeting the cumulative % threshold at each instalment date |

| Example impact | Shortfall Rs 50,000 from April to June (3 months) = Rs 1,500 interest | June instalment shortfall Rs 20,000 for 3 months = Rs 600 interest |

425 interest applies during the year at each instalment stage. 424 interest applies after March 31 if total advance tax paid was less than 90% of assessed tax — it continues until full payment. Senior citizens without business income are exempt from both 424 and 425.

The 90% safe harbour: if you pay at least 90% of your full year assessed tax as advance tax by March 31 (across all four instalments combined), Section 424 interest does not apply. You can make up the remaining 10% as self-assessment tax when filing ITR without 424 interest.

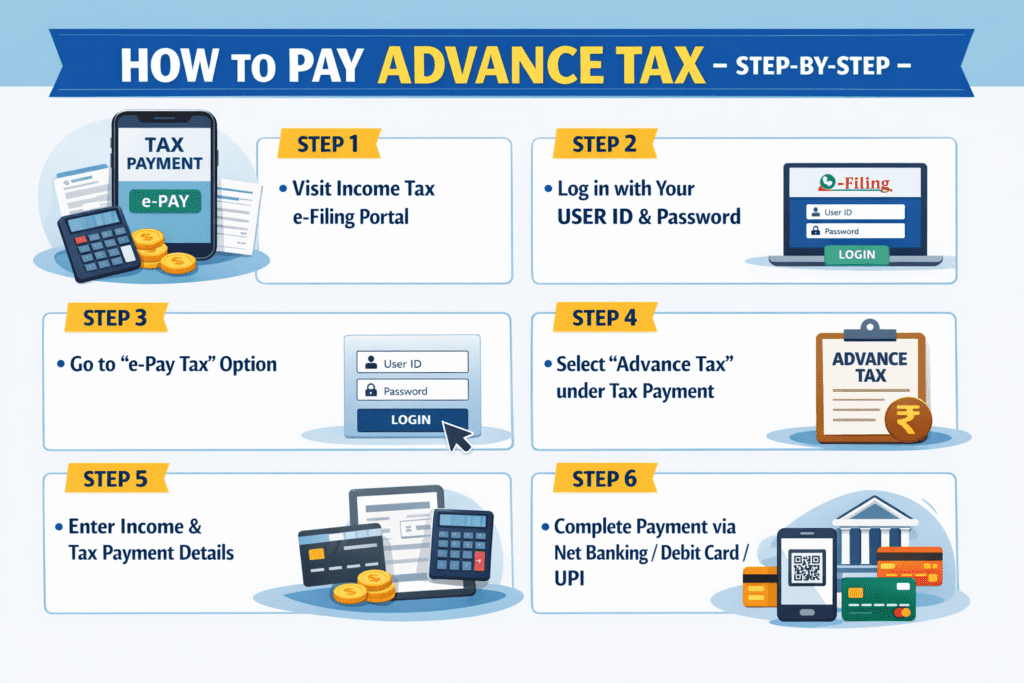

5. How to Pay Advance Tax — Step-by-Step

Advance tax is paid using Challan (also called ITNS) on the official Income Tax e-filing portal.

| Step | Action | Details |

| Step 1 | Login to e-Filing portal | Go to www.incometax.gov.in. Login with PAN and password. |

| Step 2 | Navigate to e-Pay Tax | “e-File” > “e-Pay Tax” > “New Payment”. Or go directly to the payment section. |

| Step 3 | Select correct details | Tax Applicable: Income Tax (Other than Companies) — code 0021. Type of Payment: Advance Tax — code 100. Assessment Year: 2026-27 (for financial Year 2025-26). |

| Step 4 | Enter amount and pay | Enter the instalment amount. Select payment method: Net Banking, Debit Card, UPI, RTGS/NEFT, or Over-the-Counter (bank). Complete payment. |

| Step 5 | Download challan | Save the Challan Identification Number (CIN) and download the challan receipt. You will need BSR code and challan serial number when filing ITR. |

| Step 6 | Verify in Form 26AS | After 2-3 days, check Form 26AS on the portal to confirm the advance tax payment is reflected against your PAN. |

The Challan details to remember: Assessment Year for advance tax on financial Year 2025-26 is AY 2026-27. Major head: 0021 (Income Tax, Other than Companies). Minor head/Type: 100 (Advance Tax). Enter the correct Assessment Year — a wrong AY entry requires a correction request.

Income Tax India 2026 : A Complete Guide

6. Frequently Asked Questions

Q1: What are the advance tax due dates for FY 2026-27?

Advance tax for the Tax Year 2026-27 (FY 2026-27, AY 2027-28) must be paid in 4 instalments: (1) June 15, 2026 — at least 15% of estimated full-year tax. (2) September 15, 2026 — at least 45% cumulative. (3) December 15, 2026 — at least 75% cumulative. (4) March 15, 2027 — 100% cumulative. Taxpayers under presumptive taxation (58) pay 100% in one instalment by March 15, 2027.

Q2: Who is required to pay advance tax?

Any taxpayer whose estimated income tax liability for the financial year exceeds Rs 10,000 after deducting TDS and TCS must pay advance tax. This includes salaried employees with additional income (rent, interest, capital gains), freelancers, self-employed professionals, and business owners. Resident senior citizens (60+ years) without business or professional income are EXEMPT from advance tax.

Q3: What is Section 425 interest and how is it calculated?

Section 425 interest is charged when advance tax instalments are not paid on time or are below the required cumulative percentage. Interest rate: 1% per month or part of month on the shortfall amount. Duration: 3 months for June, September, and December shortfalls; 1 month for March shortfall. No 425 interest if advance tax paid on June 15 is at least 15% of full year tax, September 15 at least 45%, December 15 at least 75%, March 15 at 100%.

Q4: What is Section 424 interest and how is it different from 425?

Section 424 applies when the total advance tax paid by March 31 is less than 90% of the assessed tax for the year. It starts from April 1 of the assessment year and continues at 1% per month until the full tax is paid. Section 425 applies during the year for missed or short instalments. Together, they cover both during-the-year defaults (425) and post-year-end shortfalls (424).

Q5: Do salaried employees need to pay advance tax?

Salaried employees whose employer deducts TDS on full salary generally do not need to pay advance tax — their TDS covers the full liability. However, if you have additional income beyond salary (rental income, FD interest, capital gains from stocks or mutual funds) and your total tax liability after TDS exceeds Rs 10,000, you must pay advance tax on that additional income. Calculate your total tax liability (salary + additional income) and subtract TDS deducted — if the balance exceeds Rs 10,000, pay advance tax on the balance in the 4-instalment schedule.

Q6: Can I pay all advance tax in the last instalment in March?

For most taxpayers (non-presumptive), paying all advance tax only in March means Section 425 interest will apply for the missed June, September, and December instalments. You can legally choose to pay 100% by March 15 but will incur 425 interest for the earlier missed instalments. However, for taxpayers under presumptive taxation (Section 58), the entire advance tax in one instalment by March 15 is the prescribed method with no penalty.

Q7: What happens if I overpay advance tax?

If you overpay advance tax — your total advance tax paid exceeds your actual tax liability when assessed — the excess amount will be refunded to you back. When you file your ITR, the system calculates the refund (excess advance tax + TDS minus actual tax liability) and credits it to your bank account after ITR processing. Overpaying advance tax has no penalty. The refund is processed by the IT Department after ITR filing and verification.

Q8: How do I verify my advance tax payment?

After paying advance tax via Challan , the payment reflects in Form 26AS (Tax Credit Statement) within 2-3 working days. To verify: Login to incometaxindia.gov.in > e-File > Income Tax Returns > View Form 26AS. Look for the advance tax entry showing BSR code, challan serial number, date, and amount. When filing ITR, enter these details in the tax payment section to claim credit for advance tax paid. Always save the challan receipt with BSR code and serial number.

Conclusion

Advance tax is not complicated — it is simply a requirement to pay your estimated tax in four quarterly instalments rather than all at once at year end. The key points:

- Rs 10,000 threshold: Tax liability after TDS above Rs 10,000 means advance tax is mandatory.

- Four dates: June 15 (15%), September 15 (45%), December 15 (75%), March 15 (100%). Mark your calendar.

- 1% per month: Interest under 425 for instalment shortfalls, 424 for total underpayment after March 31.

- Senior citizen exemption: Resident senior citizens with no business income are fully exempt.

- Challan online: Pay on www.incometax.gov.in. Select Assessment Year , Type: Advance Tax (100).

For tax slab rates to calculate your estimated liability: Income Tax Slabs FY 2025-26: New & Old Regime Rates 2026

Must read Mutual Funds India 2026: Complete Beginner’s Guide

Author

CA Ajay Khandelwal is a Chartered Accountant and financial expert with over 21 years of experience in taxation, compliance, and business advisory. As a key expert at AspirixWriters, he provides practical insights on income tax, financial planning, and regulatory matters, helping readers make informed financial decisions.

Author profile CA. Ajay Khandelwal

Disclaimer

This article is for educational and informational purposes only. It is not personal tax advice. Advance tax liability depends on individual income, TDS deducted, and applicable deductions. Interest rates under Sections 424 and 425 are based on the IT Act 2025. Please consult your Chartered Accountant for your specific advance tax calculation and payment schedule.

References

- Income Tax Department — FAQs on interest under Section 423, 424, 425 and 426 | Advance tax instalment percentages | Senior citizen exemption | Section 425 thresholds (15%/45%/75%/100%) | incometaxindia.gov.in

- Income Tax Department — Tax Calendar: Payment of Advance Tax | Due dates June 15 / September 15 / December 15 / March 15 | Challan payment guide | incometaxindia.gov.in —

- Income Tax Act 2025 (Act 30 of 2025), egazette.gov.in | Sections 403-410 — Advance Tax provisions | Section 403 liability | Section 404 conditions | Presumptive taxation advance tax under Sec.58 — https://egazette.gov.in

How to Classify Your AI System Under the EU AI Act (Guide)

EU AI Act Risk Classification Step-by-Step How Do I Classify My AI System Under the…

My SaaS Uses ChatGPT — Am I Regulated Under the EU AI Act? AI Act ChatGPT Integration Compliance

EIU AI Act ChatGPT Integration Compliance Rohan built a customer-support SaaS tool in Pune. Under…

EU AI Act Compliance for Indian SaaS Startups (No Team Needed)

How Can an Indian SaaS Startup Comply with the EU AI Act Without Hiring a…

Does the EU AI Act Apply to My Company If I’m Not Based in Europe?

Does the EU AI Act apply to Non-EU Companies Quick Answer Yes — in most…

The EU AI Act Explained (2026): A Complete Guide for Businesses, Startups & AI Professionals

The EU AI Act Explained Reviewed Against: Regulation (EU) 2024/1689 and official European Commission guidance….

How to Check Is Your AI System High-Risk Under the EU AI Act (2026)

Is Your AI System High-Risk Under the EU AI Act (2026)? Rohan is a product…