One Gives Stability. The Other Builds Long-Term Wealth. Most Salaried Employees Need Both.

If you are first time home buyer and don’t know how to save thousands here is smart guide for you How to Save Tax on Home Loan 2026: Complete Guide for First-Time Buyers

Every month, salaried employees across India face the same question:

“Should I invest my savings in FD or Mutual Funds?”

For decades, Fixed Deposits (FDs) were the default investment choice because they offered predictable returns and stability. But in 2026, rising inflation, changing tax rules, and long-term financial goals are pushing many salaried professionals to explore mutual funds and SIP investing.

The real question is not:

- FD or Mutual Fund.

It is:

- Which investment is better for your financial goal, time horizon, and risk tolerance?

This guide explains:

- FD vs Mutual Fund returns,

- SIP investing,

- taxation,

- inflation impact,

- risks,

- and the best investment strategy for salaried employees in India.

What Is a Fixed Deposit (FD)?

A Fixed Deposit is a traditional investment product offered by banks, post offices, and NBFCs where you deposit money for a fixed tenure at a predetermined interest rate.

The maturity amount is known in advance.

How Fixed Deposits Work

- You invest a lump sum amount

- The bank pays fixed interest

- Money remains invested for a chosen period

- You receive principal + interest at maturity

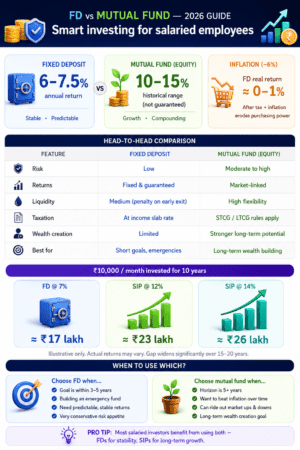

As of 2026, most major Indian banks offer approximately 6%–7.5% annual FD interest rates depending on tenure and institution.

Advantages of FDs

Stable and Predictable Returns

FDs are considered relatively stable investments when placed with regulated institutions.

Guaranteed Maturity Amount

You know the maturity value in advance.

Suitable for Conservative Investors

FDs may work well for:

- emergency savings,

- short-term goals,

- retirees,

- and highly risk-averse investors.

Disadvantages of FDs

Inflation Reduces Real Returns

Over long periods, inflation can significantly reduce purchasing power.

Interest Income Is Taxable

FD interest is taxed according to your income slab.

Limited Wealth Creation Potential

FDs may struggle to generate strong inflation-adjusted long-term growth.

What Is a Mutual Fund?

A Mutual Fund pools money from multiple investors and invests it into:

- equities,

- debt instruments,

- government securities,

- or mixed assets.

The fund is managed professionally by a fund manager.

How Mutual Funds Work

Investors buy units of the mutual fund scheme. The value of these units changes depending on market performance.

Major categories include:

- Equity Funds

- Debt Funds

- Hybrid Funds

- Index Funds

- ELSS Funds

Benefits of Mutual Funds

Better Long-Term Growth Potential

Historically, diversified equity mutual funds have offered stronger long-term growth potential than traditional fixed-income investments, though returns vary across market cycles.

SIP Flexibility

You can start SIPs with small amounts like ₹500–₹1,000 monthly.

Power of Compounding

Long-term SIP investing allows returns to compound over time.

Better Inflation Protection

Equity mutual funds have historically performed better than inflation over long periods.

Risks of Mutual Funds

Market Fluctuations

Mutual fund values can rise or fall depending on market conditions.

No Guaranteed Returns

Unlike FDs, mutual fund returns are market-linked.

Requires Patience and Discipline

Short-term volatility is normal in equity investing.

FD vs Mutual Fund — Key Differences Explained

| Feature | Fixed Deposit | Mutual Fund |

| Risk | Low | Moderate to High |

| Returns | Fixed | Market-linked |

| Liquidity | Medium | Higher flexibility |

| Taxation | Interest taxed at slab rate | Depends on fund type |

| Inflation Protection | Limited | Better long-term growth potential |

| Wealth Creation | Limited | Stronger long-term potential |

| Suitable For | Conservative investors | Long-term investors |

Which Gives Better Returns in 2026?

FD Average Returns

Most major Indian banks currently offer:

- approximately 6%–7.5% annual FD returns.

However, after:

- taxation,

- and inflation,

real returns can become relatively modest over long periods.

Mutual Fund Average Returns

Historically:

| Fund Type | Historical Long-Term Range* |

| Equity Mutual Funds | ~10–15% annualised |

| Hybrid Funds | ~8–11% |

| Debt Funds | ~6–8% |

Historical ranges are illustrative only and do not guarantee future returns.

Why Inflation Matters

This is one of the biggest differences between FD and Mutual Fund investing.

If inflation averages around 6%:

- a 6.5% FD may generate limited real growth after tax.

Over long periods, inflation can significantly reduce purchasing power.

This is one reason why many salaried employees use SIPs for long-term goals instead of relying only on FDs.

SIP vs FD — Which Is Better for Monthly Salary Earners?

Benefits of SIP for Salaried Employees

Builds Investing Discipline

SIPs automatically invest money every month from salary.

Rupee Cost Averaging

You buy more units when markets fall and fewer when markets rise.

Low Starting Amount

Most SIPs start with ₹500–₹1,000 monthly.

Long-Term Compounding

Small monthly investments can grow significantly over long periods.

For a detailed explanation, read:

Systematic Investment Plans (SIPs) are one of the smartest ways to invest in mutual funds regularly and build long-term wealth. This simple 2026 guide explains how SIP works, its benefits, monthly investment strategy, and how a SIP calculator helps estimate future returns based on your investment amount, duration, and expected growth rate.

When FD Makes More Sense

FDs may be suitable if:

- your goal is within 3–5 years,

- you need predictable returns,

- or you are building an emergency fund.

Examples include:

- emergency savings,

- travel fund,

- short-term purchases,

- and house down payment planning.

Tax Benefits — FD vs Mutual Fund

Tax on FD Interest

- FD interest is taxable according to your income slab.

- Banks may deduct TDS if prescribed thresholds are crossed.

Taxation on Mutual Funds

Mutual fund taxation depends on:

- fund type,

- holding period,

- and applicable tax provisions.

Under the current framework:

- equity mutual funds are subject to short-term and long-term capital gains taxation rules,

- while debt fund taxation depends on classification and applicable provisions.

ELSS vs Tax Saving FD

| Feature | ELSS Fund | Tax Saving FD |

| Lock-in Period | 3 Years | 5 Years |

| Return Type | Market-linked | Fixed |

| Growth Potential | Better long-term potential | Lower but predictable |

| Tax Deduction | Section 123 (old Section 80C equivalent — old regime) | Section 123 |

ELSS carries market risk but has historically offered stronger long-term growth potential compared to traditional tax-saving FDs.

Which Investment Is Better for Different Salaried Employees?

Beginners

Beginners with long-term goals may consider starting SIPs gradually through diversified mutual funds.

Related read:

Mutual funds are one of the best investment options for beginners in India because they offer professional fund management, diversification, and flexible SIP investing. If you are wondering why choose mutual funds, they help investors start with small amounts while building long-term wealth and reducing risk compared to direct stock investing. Mutual funds also help beat inflation and achieve financial goals more effectively in 2026.

Conservative Investors

FDs may suit:

- retirees,

- highly risk-averse investors,

- and short-term savers.

Young Professionals

Young salaried employees with long investment horizons may benefit more from long-term SIP compounding.

High-Income Employees

Many high-income professionals use:

- FDs for stability,

- and mutual funds for long-term growth

as part of a diversified investment strategy.

Real Example — ₹10,000 Monthly Investment for 10 Years

| Investment Type | Estimated Value After 10 Years |

| FD at 7% p.a. | ~₹17 lakh |

| SIP at 12% annualised return | ~₹23 lakh |

| SIP at 14% annualised return | ~₹26 lakh |

Illustrative calculations only. Actual returns may vary.

Over 15–20 years, the difference can widen substantially because of compounding.

Can You Invest in Both FD and Mutual Funds?

Yes — and for many salaried employees, this may be the more balanced approach.

Many investors choose to:

- keep a portion of savings in FDs or liquid funds for safety,

- and invest long-term money through SIPs for growth.

This helps balance:

- liquidity,

- stability,

- and long-term wealth creation potential.

Common Mistakes Salaried Employees Make

1. Keeping all money in savings accounts

Savings accounts often generate very low real returns after inflation.

2. Investing only in FDs

Over long periods, inflation can significantly reduce purchasing power.

3. Stopping SIPs during market falls

Historically, disciplined long-term investing has benefited from market recoveries over time.

4. Ignoring Financial Planning

Investments should align with:

- financial goals,

- risk tolerance,

- and time horizon.

Expert Recommendation — What Should Salaried Employees Choose in 2026?

There is no single investment suitable for everyone.

A practical approach many investors follow:

- safer instruments like FDs or liquid funds for emergency needs,

- and diversified mutual fund SIPs for long-term goals.

The ideal allocation depends on:

- age,

- income stability,

- family responsibilities,

- and risk appetite.

Related Reads You Should Not Miss

- Mutual Funds or Fixed Deposits: Which Grows Your Money Faster?

- Why Beginners Should Choose Mutual Funds in India

- How SIP Works: A Simple Guide with SIP Calculator Monthly for 2026

Why Trust Aspirix Writers for Financial Content?

At Aspirix Writers, we focus on:

- simplified finance education,

- research-based investment content,

- updated taxation insights,

- and beginner-friendly financial guides for Indian readers.

Our goal is to make finance easier to understand without unnecessary jargon.

Frequently Asked Questions

Is FD safer than Mutual Funds?

FDs are generally considered more stable because returns are fixed and not directly affected by market fluctuations.

Can SIP give better returns than FD?

Historically, diversified equity SIPs have offered stronger long-term growth potential than traditional FDs, though returns are not guaranteed.

Which is best for beginners: FD or Mutual Fund?

Beginners with very low risk tolerance may prefer FDs initially, while long-term investors may consider starting SIPs gradually.

Are Mutual Funds risky for salaried employees?

Mutual funds carry market risk, especially equity funds. However, longer holding periods can reduce the impact of short-term volatility.

Can I lose money in Mutual Funds?

Yes. Mutual fund values can fall temporarily depending on market conditions.

Is FD good for long-term investment?

FDs may provide stability, but long-term inflation can reduce real purchasing power over time.

Should I invest salary in SIP every month?

Many salaried employees use SIPs to automate disciplined long-term investing from monthly income.

Final Thoughts

FDs and Mutual Funds are not competitors. They solve different financial needs.

FDs help provide:

- stability,

- liquidity,

- and predictable returns.

Mutual fund SIPs help provide:

- long-term growth potential,

- inflation protection,

- and wealth creation opportunities.

For many salaried employees, the better strategy is not choosing one over the other completely — but using both wisely based on financial goals, investment horizon, and risk tolerance.

Disclaimer: This article is for educational and informational purposes only and should not be treated as personal financial advice. Mutual fund investments are subject to market risks. Returns are not guaranteed and past performance is not indicative of future results. Tax provisions are subject to amendments. Investors should evaluate their goals, risk tolerance, and investment horizon carefully or consult a SEBI-registered Investment Advisor before investing.