Last Updated: May 23, 2026

Last Updated: May 2026

Introduction

Buying a home is one of the biggest financial decisions for Indian families. Along with ownership and long-term wealth creation, many taxpayers also look for income tax benefits on home loans. However, after the introduction of the new tax regime, confusion has increased regarding whether deductions on home loans are still available.

Many taxpayers continue to claim deductions without understanding the differences between the old and new tax regimes. Others assume that all housing loan tax benefits have been removed completely. The reality is more nuanced.

This guide explains home loan tax deduction under new tax regime 2026, including Section 22 (earlier section 24) home loan deduction rules, interest deduction availability, self-occupied property treatment, rental property benefits, and key differences between the old and new regimes.

Understanding the New Tax Regime

The new tax regime was introduced to simplify income tax calculations by offering lower slab rates while removing many deductions and exemptions available under the old regime.

Under the new regime, taxpayers generally cannot claim:

- Section 123 deductions (earlier Section 80C under the 1961 Act)

- HRA exemption

- Home loan principal repayment deduction for self-occupied property

- Many tax-saving investment benefits

However, some home loan related deductions may still be available for rented or let-out properties under applicable provisions.

Can You Claim Home Loan Tax Benefits Under the New Tax Regime?

The answer depends on the type of property.

1. Self-Occupied Property

If the property is self-occupied, taxpayers under the new tax regime cannot claim:

- Section 123 deduction on principal repayment (corresponding to old Section 80C)

- Housing loan interest deduction for self-occupied property under Section 22 (earlier section 24)

Further, loss from house property for a self-occupied house cannot be adjusted against salary or other income under the new tax regime.

As a result, most traditional tax benefits linked to self-occupied home loans are not available under the new regime.

2. Let-Out / Rented Property

For rented or let-out properties, certain deductions may still be available under both tax regimes.

Taxpayers may claim:

- Housing loan interest deduction against rental income

- Municipal taxes actually paid

- 30% standard deduction on annual value as per applicable provisions

However, set-off of house property loss against other income is not available under the new tax regime.

Housing Loan Interest Deduction Explained

Under the Income-tax Act, 2025, Section 22(earlier section 24) governs deductions related to income from house property, including housing loan interest deduction.

Under the Old Tax Regime

Self-Occupied Property

- Housing loan interest deduction is generally available up to ₹2 lakh per year, subject to applicable conditions.

Let-Out Property

- Actual housing loan interest may be claimed against rental income as per applicable provisions.

Under the New Tax Regime

Self-Occupied Property

- Housing loan interest deduction for self-occupied property is not available.

- Loss from house property cannot be adjusted against salary or other income.

Let-Out Property

- Housing loan interest deduction is still available against rental income.

- set-off of house property loss against other income is not available under the new tax regime.

Taxpayers should compare both tax regimes carefully before making a final choice.

Housing Loan Interest Deduction: Important Conditions

To claim housing loan interest deduction where applicable:

- Loan must be taken for purchase, construction, repair, or renovation of house property

- Interest certificate from lender should be available

- Construction should be completed within prescribed timelines for maximum deduction eligibility

- Property ownership documents should be properly maintained

Home Loan Principal Repayment Deduction

Under the old tax regime, repayment of home loan principal qualifies for deduction under Section 123 of the Income-tax Act, 2025 (corresponding to old Section 80C), subject to the overall prescribed limit.

However, under the new tax regime:

- Section 123 deductions are not available

- Home loan principal repayment deduction cannot usually be claimed

This is one of the key differences between the old and new tax regimes.

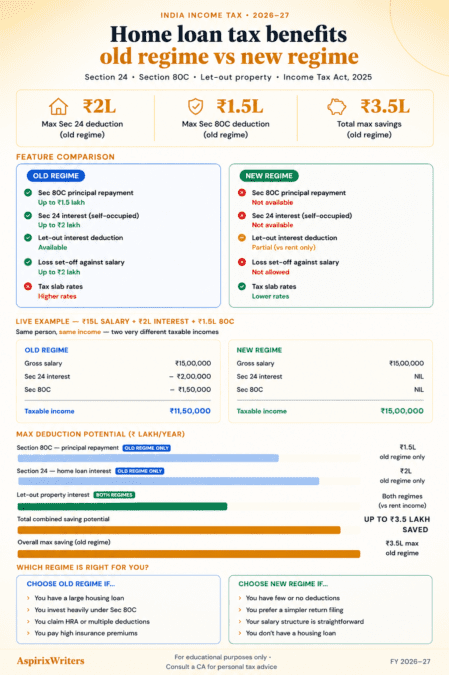

Old vs New Tax Regime: Home Loan Benefits Comparison

| Feature | Old Tax Regime | New Tax Regime |

|---|---|---|

| Section 123 deduction for principal repayment (earlier Section 80C) | Available subject to applicable limits | not available |

| Housing loan interest deduction for self-occupied property | Available up to ₹2 lakh subject to conditions | not available |

| Housing loan interest deduction for let-out property | Available against rental income | Available against rental income, but set-off restrictions apply |

| Tax-saving deductions and exemptions | Most deductions available | Many deductions and exemptions not available |

| Tax slab rates | Higher | Lower |

When Can the Old Tax Regime Be More Beneficial?

The old tax regime may be more suitable if:

- You have a large home loan

- You claim multiple tax deductions

- You invest significantly under Section 123 (earlier Section 80C)

- You pay high health or life insurance premiums

- You claim HRA and other exemptions

On the other hand, the new tax regime may benefit taxpayers who:

- have fewer deductions,

- have simpler salary structures,

- do not make significant tax-saving investments,

- or prefer lower tax slab rates with simpler tax filing.

Example

Suppose a taxpayer has:

- Annual salary: ₹15 lakh

- HRA Deduction : 4.25 lakh

- Home loan interest: ₹2 lakh

- Section 123 investments (earlier Section 80C): ₹1.5 lakh

- Section 126 deduction : ₹50,000

Under the old tax regime, these deductions may help reduce taxable income significantly and tax will be lower than new regime

Under the new tax regime, many of these deductions are not available, although tax slab rates are lower.

Therefore, the better option depends on the taxpayer’s income, deductions, and overall tax planning.

Common Mistakes Taxpayers Make

1. Choosing New Regime Without Calculation

Many taxpayers select the new regime assuming lower tax automatically means lower liability.

2. Ignoring Housing Loan Benefits

Home loan deductions can substantially reduce taxable income under the old regime.

3. Not Reviewing Let-Out Property Rules

Rental property treatment differs significantly under tax provisions.

4. Forgetting Interest Certificates

Proper documentation is essential for claiming eligible deductions.

Should You Choose Old or New Regime?

There is no single answer that suits everyone.

Taxpayers with higher deductions — especially home loan interest and Section 123 investments (earlier Section 80C) — may often benefit more from the old tax regime.

On the other hand, taxpayers with fewer deductions may prefer the lower tax rates and simpler structure of the new regime.

Before filing your income tax return, it is advisable to compare both regimes carefully based on your actual income and eligible deductions.

Basics of Rental Income & Housing Loan Tax Benefits

Rental Income

As per Section 20 of Income Tax Act, 2025, Rental Income from a House Property is treated as Income of the owner of the property. Even if there is a commercial property, its rental income is taxable under this section as Income from House Property as there is no separate provision for rent from Commercial property.

Deemed Rental Income

If a person has more than 2 house properties and none of them is let out, still only 2 of them can be treated as self-occupied property and remaining are deemed to be let out and deemed rental income is to be included in taxable income as per the provisions of Income Tax Act, 2025.

Deductions from Rental Income

There are 3 deductions allowed from rental income. Municipal Tax Paid for property, like, House Tax, are straight away allowed as deduction from rent. Further 30% of the balance amount is allowed as Standard Deduction. Moreover, any interest paid on Housing Loan is allowed as deduction subject to some conditions.

FAQs on Rental Income and Interest on Housing Loan

Is housing loan interest deduction available under the new tax regime?

For self-occupied property, housing loan interest deduction is not available under the new tax regime. However, for rented or let-out property, interest deduction may still be claimed against rental income subject to applicable rules.

Can I claim principal repayment deduction under the new tax regime?

No. Section 123 deductions (corresponding to old Section 80C deductions) are not available under the new tax regime.

What is the maximum housing loan interest deduction under the old regime?

For self-occupied property, housing loan interest deduction is generally available up to ₹2 lakh per year subject to prescribed conditions.

Is housing loan interest deduction available for rented property?

Yes. Housing loan interest may generally be claimed against rental income for let-out properties under both tax regimes, although restrictions on set-off of losses may apply under the new regime.

Is the 30% standard deduction on rental income available under the new regime?

Yes. The 30% standard deduction on rental income is generally available under both the old and new tax regimes.

Disclaimer

This article is for educational and informational purposes only and should not be considered legal, tax, or financial advice. Tax provisions may change based on amendments, notifications, and judicial interpretations. Readers should consult his Chartered Accountant or tax professional for personalised advice.

CA Ajay Khandelwal is a Chartered Accountant and financial expert with over 21 years of experience in taxation, compliance, and business advisory. As a key expert at AspirixWriters, he provides practical insights on income tax, financial planning, and regulatory matters, helping readers make informed financial decisions.

Author Profile CA. Ajay Khandelwal

Reference

Complete Guide to Income Tax in India for 2026

Income Tax Calculator 2026: New vs Old Regime Guide

Income Tax Calculator 2026 New vs Old Regime — Step-by-Step Calculation at 5 Income Levels…