Last Updated: March 30, 2026

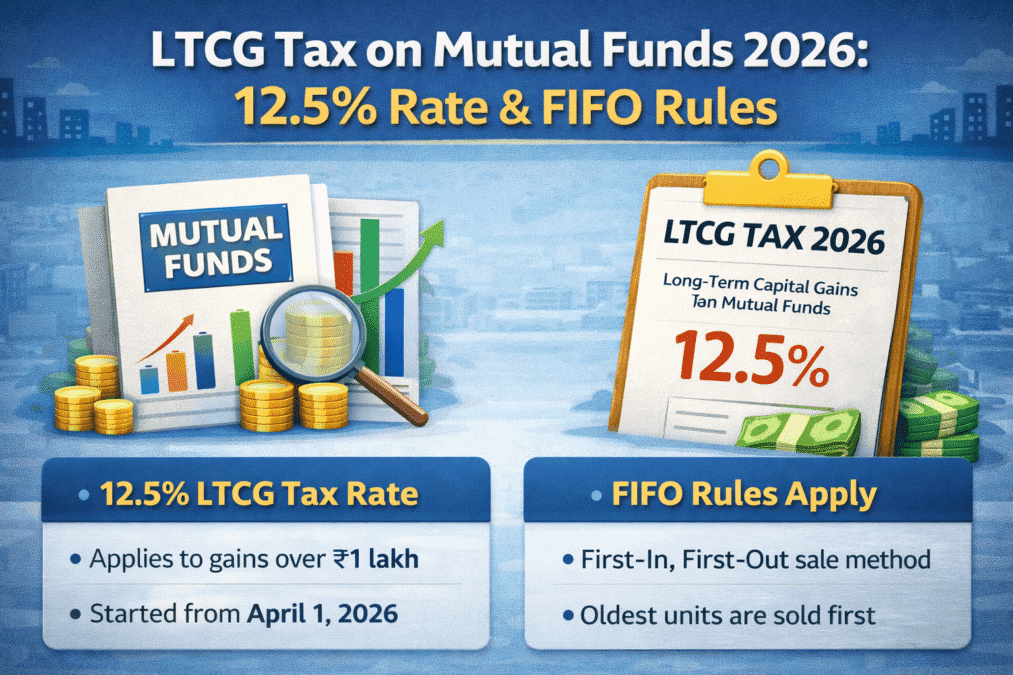

LTCG Tax on Mutual Funds 2026

12.5% Rate, Rs 1.25L Exemption, FIFO for SIP and Tax Harvesting Strategy

Part of the Income Tax India 2026 : Income Tax India 2026 : A Complete Guide

Rohan invested Rs 10,000 per month in an equity mutual fund via SIP for 5 years. His total investment: Rs 6,00,000. Current value: Rs 11,50,000. Gain: Rs 5,50,000.

He needs Rs 4 lakh for a home down payment and decides to redeem. His question: how much tax will he pay?

The answer is not simply 12.5% on Rs 5,50,000. Because of FIFO rules, Rs 1.25 lakh annual exemption, and the way SIP redemptions work — the actual tax calculation is more nuanced. And there is one more thing most investors miss: the Section 156 rebate he has been counting on does not apply to this LTCG.

This article covers every aspect of capital gains tax on mutual funds and stocks in 2026 — rates, exemptions, FIFO for SIP, the 156 warning, and the tax harvesting strategy that can legally reduce your tax to zero on up to Rs 1.25 lakh of gains every year.

| 12.5% LTCG rate on equity MF and stocks (gains above Rs 1.25L) | 20% STCG rate on equity MF and stocks (held 12 months or less) | Rs 1.25L Annual LTCG exemption — tax-free every year | FIFO Each SIP instalment redeemed oldest-first |

Capital Gains Tax Rates — All Asset Classes

Capital gains rates for Tax Year 2026-27 are unchanged from last year.

| Asset Type | Holding Period for LTCG | LTCG Tax Rate | STCG Tax Rate | Annual LTCG Exemption |

| Equity Mutual Funds (domestic) | More than 12 months | 12.5% on gains above Rs 1.25L | 20% | Rs 1,25,000 |

| Listed Equity Shares | More than 12 months | 12.5% on gains above Rs 1.25L | 20% | Rs 1,25,000 (shared with MF) |

| Debt Mutual Funds (purch after 01.04.23) | No LTCG benefit — any period | Slab rate (no LTCG) | Slab rate | No exemption |

| Gold ETF / Gold Fund | More than 24 months | 12.5% (no indexation) | Slab rate | No exemption |

| International / US Funds (FoF) | More than 24 months | 12.5% (no indexation) | Slab rate | No exemption |

| Residential Property | More than 24 months | 12.5% without indexation | Slab rate | Section 82 reinvestment exemption |

| Unlisted Shares | More than 24 months | 12.5% | Slab rate | Within Rs 1.25L pool |

Important: The Rs 1,25,000 LTCG annual exemption is a shared pool across all assets eligible for Section 198 treatment (equity MF, listed shares, Gold ETF, international funds). It is not Rs 1.25L per asset class. Total LTCG from all these assets combined is exempt up to Rs 1.25L.

How LTCG and STCG Work for Mutual Funds

Mutual fund capital gains are calculated at the unit level, not the fund level. Each unit purchased has its own cost price and purchase date. When you redeem, the gain on each unit is either LTCG or STCG depending on how long that specific unit was held.

| Question | Answer |

| What is LTCG for equity MF? | Gain on equity MF units held MORE than 12 months. Taxed at 12.5% on total LTCG above Rs 1.25L across all equity assets. |

| What is STCG for equity MF? | Gain on equity MF units held 12 months or LESS. Taxed at flat 20% — no exemption. |

| What is the holding period base date? | Date of allotment of each unit. For SIP, each monthly instalment has its own allotment date. |

| What happens with debt MF? | Any holding period — gains taxed at slab rate. No LTCG benefit. No exemption. Finance Act 2023 removed LTCG for debt MF purchased after April 1, 2023. |

| What about hybrid / balanced MF? | If equity component is 65% or more — treated as equity fund (LTCG 12.5% after 12 months). Below 65% equity — treated as debt fund (slab rate). |

| Is there TDS on MF redemption? | For resident Indians: no TDS on equity MF redemption. Tax is self-reported in ITR. For NRIs: TDS applies at applicable rates. |

FIFO Rule for SIP — How Each Instalment is Taxed

This is the part most SIP investors do not know. When you redeem mutual fund units, they are redeemed on a First-In-First-Out (FIFO) basis — the oldest units are redeemed first. Each SIP instalment is a separate purchase with its own allotment date and cost.

FIFO Worked Example — Monthly SIP of Rs 10,000

| SIP Month | Units Allotted (example) | Allotment Date | Holding Period on April 1, 2026 | Tax Treatment if Redeemed Apr 2026 |

| April 2024 | 100 units @ Rs 100 NAV | April 5, 2024 | 24 months | LTCG — held more than 12 months |

| May 2024 | 98 units @ Rs 102 NAV | May 6, 2024 | 23 months | LTCG — held more than 12 months |

| March 2025 | 90 units @ Rs 111 NAV | March 5, 2025 | 13 months | LTCG — held more than 12 months |

| April 2025 | 88 units @ Rs 113 NAV | April 4, 2025 | 12 months exactly | LTCG — held exactly 12 months (borderline — verify the date) |

| March 2026 | 82 units @ Rs 122 NAV | March 4, 2026 | 28 days | STCG — held less than 12 months, taxed at 20% |

Key insight: in a partial redemption, FIFO means the oldest units (most likely LTCG) are sold first. In a full redemption, most units in a long-running SIP will be LTCG, but the most recent 12 months of SIP instalments will generate STCG at 20%.

For SWP (Systematic Withdrawal Plan) investors: each SWP withdrawal also follows FIFO. Units invested first are redeemed first. Long-running SWPs are therefore mostly LTCG.

For the complete SWP guide: SWP Calculator and Monthly Income Guide (MF Cluster 9)

The 156 Rebate Warning — It Does Not Apply to LTCG or STCG

This is the most widely misunderstood aspect of capital gains tax. Section 156 rebate does NOT apply to LTCG under Section 198 (equity mutual funds and stocks) or STCG under Section 196.

| Situation | Salary / Other Income | LTCG from Equity MF | 156 Rebate on Salary? | 156 Rebate on LTCG? | LTCG Tax |

| Example A | Rs 8,00,000 | Rs 2,00,000 (above Rs 1.25L = Rs 75K taxable) | Yes — salary tax reduced to zero | No — rebate not available | Rs 75,000 x 12.5% = Rs 9,375 |

| Example B | Rs 12,00,000 (salaried, new regime) | Rs 1,00,000 (below Rs 1.25L exemption) | No — 156 don’t apply (even LTCG is exempt but counted for 156 limit) | Not applicable — LTCG below exemption | Zero — within exemption |

| Example C | Rs 5,00,000 | Rs 3,00,000 (above Rs 1.25L = Rs 1.75L taxable) | Yes — salary tax = zero | No — 156 does not apply to LTCG | Rs 1,75,000 x 12.5% = Rs 21,875 |

Practical implication: even if your salary income results in zero tax because of 156 rebate, any LTCG or STCG from mutual funds or stocks is taxed separately at 12.5% or 20% respectively — with no rebate offset.

Tax Harvesting Strategy — Rs 1.25 Lakh Every Year

Tax harvesting is the practice of redeeming mutual fund units with unrealised LTCG up to Rs 1.25 lakh and immediately reinvesting the proceeds — thereby resetting the cost price and locking in the tax-free gain each year.

How Tax Harvesting Works — Step by Step

| Step | Action | Result |

| Step 1 | In March of each Tax Year, check your equity MF portfolio for unrealised LTCG (units held more than 12 months) | Identify how much LTCG is available for harvest |

| Step 2 | If unrealised LTCG is approaching or below Rs 1.25 lakh — redeem those units | No tax on redemption (within exemption limit) |

| Step 3 | Immediately reinvest the redemption proceeds into the same fund | New units are purchased at current (higher) NAV — new cost price established |

| Step 4 | Repeat every year | Each year you crystallise Rs 1.25L of gains tax-free. Compounded over 20+ years, this saves substantial tax. |

Important conditions for tax harvesting: the Rs 1.25 lakh exemption applies to the current Tax Year (April 1 to March 31). FIFO applies — you cannot selectively choose which units to redeem. Redemptions and reinvestments within the same fund may trigger exit loads — check the fund’s exit load policy before harvesting.

Example: Priya has Rs 2.3 lakh of unrealised LTCG in her equity fund in March 2027. She redeems Rs 1.25 lakh worth and immediately reinvests. She pays zero tax on the harvested gain. The remaining Rs 1.05 lakh stays invested with the new higher cost price. Next year she can harvest again.

Conclusion

Capital gains tax on mutual funds has three rules every investor must know:

- LTCG at 12.5% after 12 months on equity MF and stocks — but first Rs 1.25L is tax-free every year

- FIFO applies to every SIP redemption — oldest units first. Recent 12 months of SIP will be STCG at 20%.

- 156 rebate does NOT reduce LTCG tax — your salary tax benefit and LTCG tax are calculated separately.

For the complete guide to SIP investing and its tax treatment: SIP In Mutual Funds 2026: How It Works, Calculator & Best Plans

For SWP investors and monthly income planning: SWP Calculator 2026: Monthly Income From Mutual Funds After Retirement

For the complete income tax guide: Income Tax India 2026 : A Complete Guide

FAQs

Q1: What is the LTCG tax rate on mutual funds in 2026?

Long Term Capital Gains (LTCG) on equity mutual funds (held more than 12 months) are taxed at 12.5% on gains exceeding Rs 1,25,000 per financial year. Gains up to Rs 1,25,000 are exempt. For debt mutual funds purchased after April 1, 2023, there is no LTCG benefit — gains are taxed at slab rate for any holding period.

Q2: What is the STCG tax rate on mutual funds in 2026?

Short Term Capital Gains (STCG) on equity mutual funds (held 12 months or less) are taxed at a flat 20% — no exemption, no threshold. STCG from ELSS funds (before 3-year lock-in expires) is not applicable because you cannot redeem ELSS within 3 years. For debt mutual funds, STCG is taxed at your income tax slab rate.

Q3: Is LTCG tax applicable on SIP mutual fund redemption?

Yes. When you redeem SIP units, LTCG or STCG is calculated for each instalment separately. Units held for more than 12 months generate LTCG (taxed at 12.5% on total LTCG above Rs 1.25L). Units held for 12 months or less generate STCG (taxed at 20%). FIFO applies — oldest units are redeemed first. For a SIP running for several years, most units at the time of redemption will qualify as LTCG — but the most recent 12 months of SIP instalments will be STCG.

Q4: Does Section 156 rebate apply to LTCG from mutual funds?

No. Section 156 rebate does NOT apply to Long Term Capital Gains taxed under Section 198 (equity mutual funds and stocks) or Short Term Capital Gains under Section 196. Even if your total income (including LTCG) is below Rs 12 lakh in the new regime, the LTCG portion will be taxed at 12.5% and the 156 rebate will only offset the non-LTCG income tax.

Q5: How is LTCG calculated for equity mutual funds?

LTCG on equity mutual funds = Sale Price minus Cost of Acquisition. For units purchased before January 31, 2018 — cost of acquisition is the higher of actual cost or the closing price on January 31, 2018 (grandfathering provision). For units purchased after January 31, 2018 — actual purchase price is the cost. No indexation benefit for equity MF LTCG.

Q6: What is debt mutual fund tax treatment in 2026?

Debt mutual funds purchased after April 1, 2023 are taxed at your income tax slab rate for any holding period — there is no LTCG benefit, no indexation benefit, and no separate tax rate. This change was made by Finance Act 2023. Debt MF purchased before April 1, 2023 retain the old treatment (LTCG after 3 years with indexation).

Q7: What is the Rs 1.25 lakh LTCG exemption on mutual funds?

Under Section 198 of the IT Act (Section 198 of IT Act 2025), the first Rs 1,25,000 of Long Term Capital Gains from equity mutual funds and listed equity shares combined is fully exempt from tax each financial year. Only gains above Rs 1,25,000 are taxed at 12.5%. This Rs 1.25 lakh limit is a shared pool — if you have LTCG from both equity MF and equity shares, the combined exemption is still Rs 1.25L.

Q8: What is tax harvesting in mutual funds?

Tax harvesting is a strategy where you redeem equity mutual fund units with unrealised LTCG up to Rs 1.25 lakh before the end of the financial year and immediately reinvest the proceeds. Since gains up to Rs 1.25L are exempt, you pay zero tax on the redemption. The new units are purchased at the current higher NAV, resetting your cost price. Done every year, this systematically reduces future LTCG tax liability. Key condition: FIFO applies — you cannot choose which units to redeem selectively. Exit loads also apply in the first 1-2 years in most equity funds — check before harvesting.

Author

CA Ajay Khandelwal is a Chartered Accountant and financial expert with over 21 years of experience in taxation, compliance, and business advisory. As a key expert at AspirixWriters, he provides practical insights on income tax, financial planning, and regulatory matters, helping readers make informed financial decisions.

Author profile CA. Ajay Khandelwal

Disclaimer

This article is for educational and informational purposes only. It is not personal tax advice. Capital gains rates, holding period rules, and exemption limits are based on Finance Act 2024, Finance Bill 2026, IT Act 2025, and incometaxindia.gov.in. Individual tax liability depends on total income, regime choice, and specific transaction details. Please consult your Chartered Accountant before making redemption or investment decisions based on tax considerations.

References

Income Tax Department — Tax Rates FY 2026-27 | Section 198 LTCG 12.5% on equity MF and shares above Rs 1.25L | Section 196 STCG 20% | Footnote (b): 156 rebate not available on LTCG/STCG | incometaxindia.gov.in —

Finance Bill 2026, Bill No. 3 of 2026 | First Schedule — IT Act 2025 rates | Section 198 (LTCG equity at 12.5% above Rs 1,25,000) | Section 196 (STCG equity at 20%) | indiabudget.gov.in — https://indiabudget.gov.in

Finance Act 2024 | LTCG rate changed from 10% to 12.5% | LTCG exemption increased from Rs 1L to Rs 1.25L | Indexation benefit removed from property and other assets | incometaxindia.gov.in — https://incometaxindia.gov.in

AMFI India — Mutual Fund taxation | LTCG and STCG on equity MF | FIFO for SIP redemptions | Tax harvesting | amfiindia.com — https://amfiindia.com

Income Tax Act 2025 (Act 30 of 2025), egazette.gov.in | Section 196 (STCG on equity) | Section 198 (LTCG on equity) | Grandfathering for pre-Jan 31, 2018 units | egazette.gov.in — https://egazette.gov.in

Mutual Funds India 2026: Complete Beginner’s Guide

Income Tax India 2026 : A Complete GuideIncome Tax India 2026 Complete GuideMutual Funds India Complete Beginner’s Guide 2026

Tax Exemption on Sale of Residential House

Section 123 Deductions 2026: Complete List of All Options

Section 123 Deductions 2026 Part of the Income Tax India 2026 : Income Tax India…

PPF Interest Rate, Limit,Withdrawal & EEE Benefits 2026

PPF Interest Rate, Limit,Withdrawal & EEE Benefits Part of the Income Tax India 2026: Income…

NPS Tax Benefit 2026

NPS Tax Benefit 2026: Section124 Rs 50K & Employer NPS Section 124 Extra Rs 50,000…

New Tax Regime vs Old Tax Regime 2026

New Tax Regime vs Old Tax Regime 2026 : Which is Better Every year between…