Last Updated: May 22, 2026

Two People. Same Salary. Completely Different Financial Futures.

Meet Riya and Arjun. Same age — 28. Same city. Same monthly take-home of ₹45,000.

Riya puts ₹5,000 every month in a Fixed Deposit. Safe, predictable, worry-free — or so she thinks.

Arjun puts the same ₹5,000 every month into a Flexi Cap mutual fund SIP and largely forgets about it.

Fast forward 20 years:

| People | Total Invested | Return Rate | Final Value |

|---|---|---|---|

| Riya (FD) | ₹12,00,000 | 7% p.a. | ₹25,81,428 |

| Arjun (Mutual Fund SIP) | ₹12,00,000 | 12% p.a. | ₹49,95,740 |

Same ₹12 lakh invested. Arjun walks away with approximately ₹24 lakh more — not because he took wild risks, but because he understood one principle of wealth creation that Riya did not.

Important Disclaimer: The 7% FD and 12% equity mutual fund return figures are illustrative only, based on long-term Nifty 50 historical averages. Mutual fund investments are subject to market risks. Actual returns vary based on fund selection, market conditions, and holding period. Past performance is not indicative of future results. Please read all scheme-related documents carefully before investing.

If you are someone who has heard about mutual funds but never quite understood why they are considered the best investment for beginners in India — this guide is exactly what you need. No jargon. No sales pitch. Just a clear, honest explanation of mutual fund advantages, backed by verified data from SEBI, AMFI, and the Income Tax Act, 2025 (as amended by the Finance Act, 2026) — the current governing law as on the date of this article.

Where India’s Mutual Fund Industry Stands Today

Before understanding why mutual funds are useful, let’s first look at how large and trusted the industry has become in India.

According to official AMFI data, the Indian mutual fund industry’s Assets Under Management (AUM) crossed approximately ₹81.92 lakh crore in 2026, while total investor folios crossed 27.5 crore. Monthly SIP contributions also crossed ₹31,000 crore, showing strong participation from retail investors across India.

More Indians are now using SIPs and mutual funds not only for investing, but also for:

- retirement planning,

- wealth creation,

- tax planning,

- child education goals,

- and long-term financial security.

Mutual funds have become one of the most preferred investment options for beginners in India because they combine:

- professional management,

- diversification,

- liquidity,

- and long-term wealth creation potential

in a single investment product.

Whether you start with ₹500 or ₹50,000 per month, mutual funds allow you to participate in equity and debt markets without needing advanced stock market knowledge.

What Is a Mutual Fund? (The Simple Version)

A mutual fund is a professionally managed pool of money collected from thousands of investors, which is then invested across a diversified basket of stocks, bonds, gold, or other assets — depending on the fund’s stated objective.

Think of it as a group of neighbours pooling money to hire a top-tier chef (the fund manager) to cook a balanced, nutritious meal for everyone. Each person contributes what they can. Everyone eats the same quality food — whether they put in ₹500 or ₹5 lakh.

Your ₹500 SIP gets the exact same professionally managed, diversified portfolio as an investor putting in ₹5 lakh. That is perhaps the most powerful and underappreciated mutual fund advantage for beginners.

Key Terms You Must Know Before Reading Further

| Term | What It Means | Practical Example |

|---|---|---|

| NAV | Per-unit price of the fund, declared once daily after market close | NAV ₹50 → ₹5,000 buys 100 units |

| Fund Manager | SEBI-certified expert managing your money full time | Decides which stocks/bonds to buy or sell |

| AUM | Total pooled money in the fund | HDFC Flexi Cap AUM exceeds ₹60,000 crore |

| Expense Ratio | Annual fee for managing the fund (deducted from NAV daily) | 1% on ₹1,00,000 = ₹1,000/year |

| SIP | Auto-debit investment on a fixed date monthly | ₹2,000 deducted on the 5th of every month |

| Exit Load | Fee for withdrawing within a specified period | 1% charge if you redeem within 1 year |

| ELSS | Equity fund eligible for deduction under Section 123, ITA 2025 | ₹1.5L invested → up to ₹46,800 tax saved (old regime, 30% slab) |

| AMFI | Industry body that oversees mutual fund distributors | Publishes verified fund data free at amfiindia.com |

How a Mutual Fund Actually Works — In 4 Simple Steps

Step 1: You Invest

You pick a fund and instruct your bank to transfer ₹1,000 every month via SIP. Minimum SIP starts at just ₹500 in most funds.

Step 2: Your Money Joins a Larger Pool

Thousands of investors contribute to the same fund. This combined amount is the AUM — managed collectively for the benefit of all unit holders.

Step 3: A SEBI-Registered Fund Manager Invests It

A qualified fund manager and their research team allocate this pool across stocks, bonds, or other assets according to the fund’s stated mandate. Your small contribution gets the same quality allocation as large investors.

Step 4: Your Wealth Compounds Over Time

As the underlying portfolio grows, your NAV increases. You can redeem (sell) your units on any business day at the prevailing NAV.

A Real Compounding Illustration

One of the biggest advantages of mutual funds is the power of long-term compounding through SIPs.

| SIP Amount | Duration | Total Invested | Estimated Value at 12% CAGR | Wealth Created |

|---|---|---|---|---|

| ₹3,000/month | 5 years | ₹1,80,000 | ~₹2.47 lakh | ~₹67,000 |

| ₹3,000/month | 10 years | ₹3,60,000 | ~₹6.97 lakh | ~₹3.37 lakh |

| ₹3,000/month | 15 years | ₹5,40,000 | ~₹15.14 lakh | ~₹9.74 lakh |

| ₹3,000/month | 20 years | ₹7,20,000 | ~₹29.97 lakh | ~₹22.77 lakh |

| ₹3,000/month | 25 years | ₹9,00,000 | ~₹56.93 lakh | ~₹47.93 lakh |

All figures are illustrative at a hypothetical 12% CAGR. Actual returns depend on market conditions and are not guaranteed.

The biggest lesson here is simple:

The investor who stayed invested for 25 years created far more wealth than the investor who invested for only 5 years — even though both invested the same amount every month.

That is the real power of compounding and disciplined SIP investing.

Types of Mutual Funds in India

SEBI has continued its ongoing rationalisation and categorisation reforms for mutual fund schemes to improve investor clarity and product transparency.

Investors should always verify the latest applicable circulars and fund classifications from SEBI before investing.

| Category | Invests In | Best For | Risk Level |

|---|---|---|---|

| Equity Funds | Shares/stocks | Long-term wealth creation | High |

| Debt Funds | Bonds & fixed-income securities | Stability and lower risk | Low–Medium |

| Hybrid Funds | Mix of equity and debt | Balanced investing | Medium |

| Index Funds | Nifty 50 / Sensex | Low-cost passive investing | Medium |

| Life Cycle Funds | Automatically changes allocation with age | Retirement planning | Varies |

Best Mutual Funds for Beginners

If you are just starting:

- Flexi Cap Funds offer professional allocation across companies of different sizes.

- Nifty 50 Index Funds provide low-cost exposure to India’s top companies.

These are generally considered suitable starting options for beginner investors.

10 Mutual Fund Advantages for Beginners — Explained With Real Numbers

Before We Begin — A Quick Comparison

What does ₹1 lakh become in 10 years?

| Investment Option | Approx. Return | Value After 10 Years | Beats ~5.5% Inflation? |

|---|---|---|---|

| Savings Account | 3–4% p.a. | ₹1,34,000–₹1,48,000 | No |

| Fixed Deposit | 6.5–7% p.a. | ₹1,88,000–₹1,97,000 | Barely |

| PPF | 7.1% p.a. (current) | ~₹1,99,000 | Marginally |

| Nifty 50 Index Fund | Market-linked (historical long-term average: 11–13% p.a.) | Varies with market | Yes, historically |

| Flexi Cap Equity Fund | Market-linked (historical long-term average: 12–15% p.a.) | Varies with market | Yes, historically |

Historically, diversified equity mutual funds and broad market indices have delivered market-linked long-term returns over extended periods, though returns are neither fixed nor guaranteed. The figures above are illustrative based on historical long-term data only and must not be construed as expected or assured returns.

Advantage 1: Professional Management at a Fraction of the Cost

A SEBI-certified fund manager and their full research team manage your investment every business day — analysing company financials, tracking macro trends, and making buy/sell decisions. The annual cost for this expertise is as low as 0.10–1% of your invested amount per year (expense ratio). No other accessible investment product in India offers this level of professional oversight at this price point.

Advantage 2: Instant Diversification

A typical equity mutual fund holds 40 to 80 different company stocks. If one company falls 50%, your portfolio absorbs a loss of approximately only 0.6–1.25%. Had you invested directly in that one company, your loss would be the full 50%. This built-in diversification is structurally impossible to replicate independently with a small investment.

Advantage 3: Start with as Little as ₹500 a Month

A ₹500 per month SIP in a Nifty 50 Index Fund gives you proportional exposure to all 50 of India’s largest companies simultaneously. AMFI data confirms that more than 60% of new SIP registrations now originate from Tier 2 and Tier 3 cities — proof that mutual funds have made meaningful wealth creation genuinely accessible at every income level.

Advantage 4: High Liquidity — Your Money Is Accessible

Most open-ended equity mutual funds process redemptions within T+2 business days with no penalty (other than exit load if redeemed within 1 year for most funds). Compare this to Fixed Deposits (penalty for premature withdrawal) or PPF (15-year lock-in). When a real financial need arises, a mutual fund gives you access without punishing you for it.

Advantage 5: SEBI-Regulated — Your Investment Is Structurally Protected

Every mutual fund operating in India must be registered under SEBI (Mutual Funds) Regulations, 1996. Your money is held in a separate trust, completely independent of the AMC’s own balance sheet. Even if the Asset Management Company were to cease operations, your invested funds remain legally protected. This is a SEBI regulatory requirement, not a marketing claim.

Advantage 6: Tax Benefits of ELSS — Explained Simply (Updated for 2026)

ELSS (Equity Linked Savings Scheme) is one of the most popular tax-saving mutual funds in India. But from 2026 onwards, the tax rules have changed under the new Income-tax Act, 2025.

Here’s what investors should know in simple language.

Can ELSS Still Save Tax in 2026?

Yes — but mainly under the old tax regime.

Under Section 123 read with Schedule XV of the Income-tax Act, 2025, eligible ELSS investments can qualify for tax deduction up to ₹1.5 lakh per year.

However:

- Under the new default tax regime, most deductions — including ELSS deductions — are not available.

- Investors usually need to opt for the old tax regime to claim this deduction.

| Tax Regime | ELSS Tax Benefit |

|---|---|

| Old Tax Regime | Deduction up to ₹1.5 lakh available |

| New Tax Regime | not available |

Simple Example

Suppose you invest ₹1.5 lakh in ELSS:

- Under the old regime, a taxpayer in the 30% slab may save up to approximately ₹46,800 including cess.

- Under the new regime, the same investment may not provide any upfront tax deduction.

That means ELSS today should not be viewed only as a tax-saving product. It is also a long-term equity investment option.

Tax on Equity Mutual Funds in 2026

When you sell an equity mutual fund, tax depends mainly on how long you held the investment.

| Type of Gain | Holding Period | Tax Rate |

|---|---|---|

| Short-Term Capital Gain (STCG) | Up to 12 months | 20% |

| Long-Term Capital Gain (LTCG) | More than 12 months | 12.5% on gains above ₹1.25 lakh |

Important Things to Remember

- Gains up to ₹1.25 lakh under LTCG are exempt every year.

- Equity mutual funds held for more than 12 months qualify as long-term investments.

- These rules apply to most equity-oriented mutual funds, including ELSS.

Example

Suppose:

- You invested ₹5 lakh in an equity mutual fund.

- After 3 years, the investment value became ₹7 lakh.

Your total profit = ₹2 lakh.

Under current LTCG rules:

- First ₹1.25 lakh → tax-free

- Remaining ₹75,000 → taxed at 12.5%

Safer Long-Term Investing Approach

Historically, diversified equity mutual funds have recovered from major market downturns over longer investment horizons, although future performance is never guaranteed.

This is why many investors prefer:

- starting early,

- investing consistently through SIPs,

- and staying invested for the long term

instead of trying to time the market repeatedly.

Advantage 7: Rupee Cost Averaging — Volatility Becomes Your Friend

A SIP automatically purchases more units when the market falls and fewer units when it rises. Over time, your average cost per unit becomes lower than the market’s average price — a mechanism called Rupee Cost Averaging.

Practical illustration:

| Month | NAV | SIP Amount | Units Purchased |

|---|---|---|---|

| Month 1 | ₹100 | ₹5,000 | 50.00 |

| Month 2 | ₹50 (market falls) | ₹5,000 | 100.00 |

| Month 3 | ₹80 (partial recovery) | ₹5,000 | 62.50 |

| Total | — | ₹15,000 | 212.50 units |

Average cost per unit: ₹70.59. Current value at ₹80 NAV: ₹17,000. You are in profit even though the market is still below its starting price. This is the mathematical benefit of SIP investing.

Advantage 8: The Compounding Effect — Time Is the Real Asset

Refer to the compounding table in the How a Mutual Fund Works section above. The core insight: the 5-year investor created ₹64,000 extra on the same monthly contribution as the 25-year investor who created ₹47 lakh extra. Same monthly amount. The only difference was time in the market.

Every year you delay starting a SIP costs you more in absolute future wealth than the year before it.

Advantage 9: Goal-Based Investing for Every Life Stage

| Goal | Time Horizon | Recommended Fund Type |

|---|---|---|

| Emergency buffer | 0–1 year | Liquid Fund or Money Market Fund |

| Home down payment | 2–3 years | Short Duration Debt Fund |

| Child’s education | 10–15 years | Flexi Cap or Large & Mid Cap Fund (SIP) |

| Tax saving (old regime only) | 3+ years | ELSS Fund |

| Retirement corpus | 20–30 years | Life Cycle Fund or Flexi Cap |

| Post-retirement income | Ongoing | SWP from Balanced Advantage Fund |

One well-structured mutual fund portfolio can address your entire financial life from age 25 onwards — without needing multiple disconnected products from multiple institutions.

Advantage 10: Complete Portfolio Transparency — By Law

Every mutual fund in India is legally required to publish its full portfolio every month, disclosing every holding, its proportion, and valuation. This information is available free of charge at AMFI’s official website. No other investment product in India — not FDs, not life insurance policies, not ULIPs — offers this level of mandated transparency to a retail investor investing ₹500 per month.

What Is SIP? A Simple Explanation

SIP — Systematic Investment Plan — is an automated instruction to your bank to transfer a fixed amount to your chosen mutual fund on a set date every month. Think of it as an EMI in reverse: instead of paying a lender, you are systematically paying your future self.

India’s SIP data as of January 2026 (AMFI):

- Active SIP accounts: 9+ crore

- Monthly SIP inflows: ₹26,400 crore

- Minimum SIP: ₹500/month

- Consecutive months of net positive equity inflows: 60+ months

How to Start a SIP — 5 Steps

Step 1 — Complete KYC (One time, 10 minutes) Your Aadhaar and PAN are all you need. Complete it free at MF Central — the AMFI-authorised KYC portal.

Step 2 — Choose Your Fund For beginners: a Flexi Cap Fund or Nifty 50 Index Fund. Check 5-year CAGR, expense ratio, and AUM at AMFI’s free website. Do not choose based solely on last year’s returns.

Step 3 — Choose a Platform Direct plans (zero distributor commission): Groww, Zerodha Coin, Paytm Money, or directly on the AMC’s website. Over 20 years, the lower expense ratio of direct plans compounds into a significant wealth difference.

Step 4 — Set Amount and Date Start with what you can invest consistently — even ₹500 works. Set the SIP date 3–5 days after your salary credit.

Step 5 — Activate Auto-Debit and Stay the Course A NACH mandate with your bank handles everything automatically. Check your portfolio once a quarter — not every day.

SEBI Mutual Fund Category Reforms 2026 — What Changed for Investors

SEBI has continued its ongoing rationalisation of mutual fund categories as part of its investor protection and product standardisation mandate under SEBI (Mutual Funds) Regulations, 1996. Key structural changes relevant to investors in 2026:

| What Changed | Earlier Position | Current Position | Impact on You |

|---|---|---|---|

| Equity minimum | 65% for select funds | 80% for focused, contra, value funds | Funds are now more “true to label” |

| Solution-oriented schemes | Children’s and Retirement Funds available | Discontinued for new subscriptions | Existing investors migrated to better-matched schemes |

| Life Cycle Funds | Did not exist | New SEBI-approved category | Automatic rebalancing by age for retirement investors |

| Portfolio overlap | No restriction | Max 50% overlap between Value and Contra funds | Better diversification across your portfolio |

| Multi Cap allocation | Flexible | Min 25% each in large, mid, small cap | Guaranteed diversification — manager cannot over-concentrate |

The new Life Cycle Fund category automatically shifts allocation from equity to debt as you age: 80–95% equity in your 20s and 30s, shifting toward balanced allocation in your 40s and 50s, and predominantly debt after 55. You manage nothing — the fund adjusts automatically.

Mutual Funds vs FD vs PPF vs Direct Stocks — Full Comparison

| Feature | Mutual Fund | Fixed Deposit | PPF | Direct Stocks |

|---|---|---|---|---|

| Expected returns | Market-linked (equity historical long-term avg: 10–15% p.a. — not guaranteed) | 6.5–7% p.a. | 7.1% p.a. (current) | Highly variable |

| Minimum investment | ₹500/month via SIP | ₹1,000 | ₹500/year | 1 share (varies) |

| Liquidity | T+2 settlement | Penalty on premature withdrawal | Locked 15 years | T+1 settlement |

| Tax on gains (equity) | LTCG 12.5% above ₹1.25L; STCG 20% | Taxed at income slab rate (up to 30%) | Tax-free on maturity | LTCG 12.5%; STCG 20% |

| Professional management | Yes — full-time SEBI-certified team | None | None | None |

| Diversification | 40–80 stocks in one fund | Zero | Government securities | Limited to your capital |

| Beats ~5.5% inflation? | Has historically — not guaranteed | Barely | Slightly above inflation | Yes, if you pick right |

| SEBI regulated? | Yes — 100% | RBI regulated | Government guaranteed | Yes — SEBI regulated |

| Suitable for beginners? | Yes — ideal starting point | Yes | Yes | No — needs deep research |

Six Costly Mistakes Beginners Make — And How to Avoid Them

Mistake 1 — Chasing last year’s top performer. A fund that returned 45% last year is not guaranteed to repeat. Study 5-year and 10-year CAGR, standard deviation, and Sharpe ratio — all freely available at amfiindia.com.

Mistake 2 — Stopping SIP when markets fall. When NAV falls, your SIP buys more units at a lower price. Stopping means you miss the most valuable accumulation window. Every investor who paused SIPs in 2008 and March 2020 has reported the same regret.

Mistake 3 — Investing across too many funds. 12 SIPs does not mean better diversification — it creates portfolio overlap and diluted returns. Two to three well-selected funds are sufficient for most beginners.

Mistake 4 — Comparing mutual funds to a winning stock story. One stock can also fall 70–90%. Mutual funds hold 40–80 stocks with full-time professional oversight. The upside of an individual stock is exciting; the downside is usually ignored until too late.

Mistake 5 — Checking the portfolio every day. Daily monitoring during volatile periods leads directly to panic-driven decisions. Quarterly portfolio reviews are sufficient.

Mistake 6 — Investing without an emergency fund. A financial emergency that forces you to redeem a mutual fund during a downturn turns a temporary paper loss into a permanent one. Always maintain 6 months of living expenses in a liquid account before committing to equity SIPs.

Key Takeaways

- Mutual funds offer professional management, diversification, and liquidity that no other accessible investment product in India simultaneously matches.

- A SIP of ₹500/month, started early and maintained consistently, builds substantial long-term wealth through compounding.

- STCG on equity-oriented fund units is now 20% under Section 196, ITA 2025 (increased from 15% under the old Act, with effect from 1 April 2026).

- LTCG on equity-oriented fund units remains 12.5% above ₹1,25,000 under Section 198, ITA 2025 — confirmed unchanged.

- ELSS deduction (Section 123 read with Schedule XV, ITA 2025) is available only under the old tax regime. Under the new default regime (Section 202), most Chapter VIII deductions including ELSS-linked investments are not available unless specifically permitted.

- Debt fund gains (units acquired after 1 April 2023) are taxed at slab rates as short-term capital gains under Section 76, ITA 2025, subject to portfolio composition — regardless of holding period.

- SEBI has continued its ongoing rationalisation of mutual fund categories to strengthen investor protection and product transparency. Check sebi.gov.in for the latest circulars applicable to your investments.

Frequently Asked Questions

1: Can I lose all my money in a mutual fund?

Mutual funds can go up and down in the short term, but a diversified equity fund spreads your money across many companies, reducing the risk of complete loss. Historically, long-term investors who stayed invested for 7–10 years have generally seen positive outcomes, though returns are never guaranteed. Mutual funds are market-linked investments and carry risk. Please read all scheme-related documents carefully before investing.

Q2: What is the minimum amount to start investing?

₹500 per month for most SIP plans. Some funds accept ₹100. There is no upper limit. Consistency matters more than the amount — ₹500 every month for 20 years will significantly outperform ₹5,000 invested once a year.

Q3: When can I withdraw my money?

On any business day for open-ended equity funds. Proceeds arrive in your bank account within T+2 working days. Liquid and debt funds usually settle in T+1. ELSS funds have a 3-year lock-in per SEBI regulations. Most equity funds charge a 1% exit load only if redeemed within 1 year.

Q4: Is it safe to invest in mutual funds in 2026 despite market uncertainty?

Indian stock markets have recovered from major crises like the 2008 financial crash and COVID-19 market fall. Investors who continued SIPs during these periods generally benefited over the long term. However, mutual funds are market-linked investments and carry risk, so always invest according to your financial goals and time horizon.

Q5: Direct plan or regular plan — which is better?

Direct plans usually have lower charges because there is no distributor commission involved. Over the long term, this can help investors save more money and earn better returns. Choose a direct plan if you can invest on your own. If you need professional guidance, a regular plan through a SEBI-registered advisor may be suitable.

Conclusion

The mutual fund advantages for beginners in India are not theoretical. They are structural, legally governed, and statistically demonstrated across decades of market data.

Whether you are a 23-year-old beginning your first job or a 40-year-old looking to accelerate retirement savings — a well-chosen mutual fund SIP is one of the most powerful and accessible wealth creation tools available in India’s financial ecosystem today.

Start with one fund. Invest consistently. Review quarterly. Increase your SIP as your income grows. Understand your tax regime clearly before making ELSS decisions. Let compounding do the rest.

The best time to have started was ten years ago. The second best time is today.

Official References

- Income Tax Act, 2025 (as amended by Finance Act, 2026) Sections 76, 123, 196, 198, 202 and Schedule XV — Capital gains taxation, ELSS deduction eligibility, new tax regime Income Tax Department — incometaxindia.gov.in

- SEBI (Mutual Funds) Regulations, 1996 — Categorisation and Rationalisation of Mutual Fund Schemes Securities and Exchange Board of India

- AMFI — Mutual Fund Industry Data and Monthly SIP Reports Home | AMFI

About the Author: CA. Ajay Khandelwal is a Chartered Accountant and financial expert with over 21 years of experience in taxation, compliance, and business advisory. He provides practical insights on income tax, financial planning, and regulatory matters to help readers make informed financial decisions.

Disclaimer

This article is for educational and informational purposes only. It does not constitute personal financial advice or a recommendation to buy or sell any specific mutual fund.

Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future results. Returns mentioned are historical and illustrative — actual returns may vary.

For personalised investment advice, consult a SEBI-registered Investment Advisor: sebi.gov.in

My SIP Is in Loss. Should I Stop Investing?

SIP in loss – Riya is a 28-year-old software engineer in Bengaluru. She started a…

Mutual Fund Vs FD? Which Is Better In 2026 for Salaried Employees

One Gives Stability. The Other Builds Long-Term Wealth. Most Salaried Employees Need Both. If you…

Mutual Funds India Complete Beginner’s Guide 2026

Mutual Funds India 2026 Complete Beginner’s Guide to Benefits, SIP, Types & SEBI New Rules…

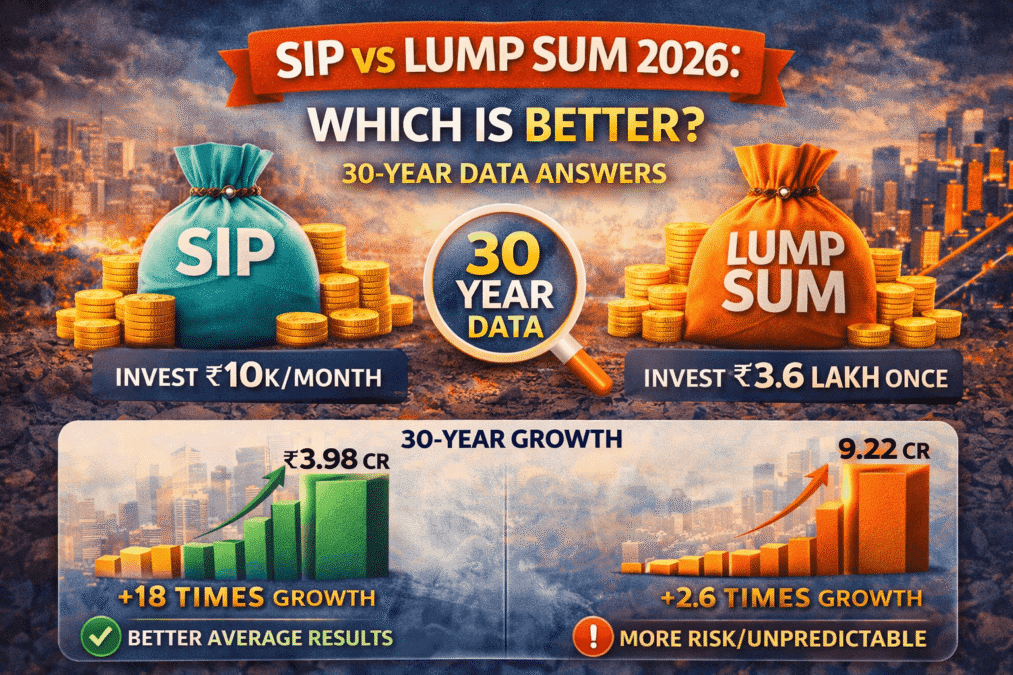

SIP vs Lump Sum 2026: Which Is Better?

SIP VS LUMP SUM 2026 SIP vs Lump Sum in Mutual Funds 2026: Which Is…

Mutual Fund Trends India 2026: AUM, SIP and Key Data

MUTUAL FUND TRENDS INDIA 2026 Mutual Fund Trends India 2026: AUM Hits Rs 82 Lakh…

Defence Sector Mutual Funds: Is It the Right Time to Invest?

Your Inbox Has a New Message. Read This Before You Act. West Asia is in…