Last Updated: April 19, 2026

SIP VS LUMP SUM 2026

SIP vs Lump Sum in Mutual Funds 2026: Which Is Better? 30-Year Data Answers

Part of our Mutual Funds India 2026 hub: Complete Guide to Mutual Funds India 2026

Priya is 32. She just got a Rs 5 lakh bonus. She is staring at her bank account wondering: do I invest it all right now, or spread it out month by month?

Her colleague Ramesh, 45, has been running a Rs 10,000 monthly SIP for years. He wonders if he would have been better off investing larger amounts whenever the market corrected.

Two smart people. Same question. Different versions of the same fundamental dilemma that every Indian investor with money to invest eventually faces.

SIP or lump sum. Which is better?

The answer, according to 30 years of Nifty data analysed by Alok Jain of Weekend Investing, is this: the difference is smaller than you think — and the method you will actually stick to is more important than the method that looks best on paper.

This article gives you the complete picture — the data, the scenarios, the tax implications, the STP solution, and a clear decision framework to choose the right approach for your specific situation in 2026.

| Rs 3.38 Cr SIP result: Rs 10K/month for 30 years | Rs 3.90 Cr Dip-buying lump sum: same total invested | -20% to +14% Lump sum return range in 2025 alone | 97% MF schemes with positive returns for SIP investors in 2025 |

1. What Exactly Is SIP and What Is Lump Sum?

Before comparing them, let us be precise about what each one is.

| Feature | SIP (Systematic Investment Plan) | Lump Sum |

| Definition | A fixed amount invested at regular intervals — typically monthly — in a mutual fund scheme | A single one-time investment of a larger amount in a mutual fund scheme |

| Minimum amount | Rs 500 per month. Some funds allow Rs 100. | Typically Rs 1,000 or more as a single investment |

| How it works | Auto-debit from your bank via NACH mandate on a fixed date every month | Single purchase at the NAV on the investment date |

| Market timing needed? | No — you invest regardless of market level | Yes — entire amount exposed at one price point |

| Who it suits best | Salaried investors, beginners, anyone building a regular savings habit | Investors with a bonus, inheritance, maturity proceeds, or property sale proceeds |

| Risk of wrong timing | Very low — spread over months and years | High — if you invest at a market peak, recovery can take years |

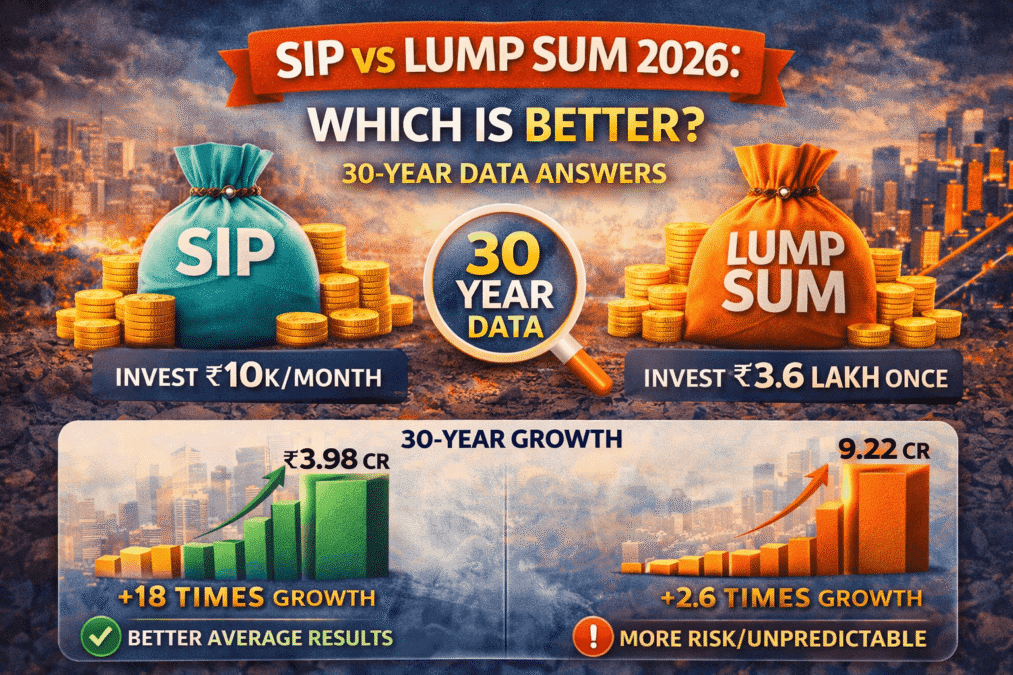

2. The 30-Year Nifty Data — Three Strategies, Same Rs 37.2 Lakh

Alok Jain, founder of Weekend Investing, ran a rigorous 30-year comparison (1995 to 2025) using Nifty 50 data. Three strategies were tested, all with identical total investments of Rs 37.2 lakh over 30 years. The results are the most important data point in this entire debate.

| Strategy | How It Works | Total Invested | Final Portfolio Value | XIRR |

| Pure Monthly SIP | Rs 10,000 every month. No timing. No decisions. Fully automatic. | Rs 37.2 lakh | Rs 3.38 crore | ~12.48% |

| Annual Dip-Based Lump Sum | Rs 1.2 lakh invested once a year — but ONLY when Nifty corrected 10%+. Cash earns 6% while waiting. | Rs 37.2 lakh | Rs 3.90 crore | ~12.41% |

| Hybrid: SIP + Lump Sum on Dips | Rs 5,000 monthly SIP + Rs 60,000 lump sum deployed when Nifty fell 10%+ in a year. | Rs 37.2 lakh | Rs 3.90 crore | ~12.45% |

The conclusion from 30 years of data: the difference between the three strategies is Rs 52,000 in XIRR terms and about Rs 52 lakh in final value — on a Rs 37.2 lakh total investment. That is a real difference. But it is not the life-changing gap that marketing materials imply.

More importantly: the dip-based strategy sounds easy in hindsight. In practice, it required the investor to hold cash earning 6% while watching the market go up — waiting for a 10% correction that might not come for 2 or 3 years. Most investors cannot do that without deploying the cash too early or too late. Behavioural execution, not mathematical theory, is what determines real-world outcomes.

As Jain noted: “Buying the dip is harder in practice than in theory. You never know the bottom. A 10% fall could turn into 20% or 30%, and many investors freeze.”

3. How Each Method Performs Across Different Market Conditions

The 30-year average is useful. But markets go through distinct phases. Here is how each approach performs in each phase.

| Market Condition | SIP Performance | Lump Sum Performance | Winner |

| Strong bull market (markets rise consistently) | Good — but buys fewer units as NAV rises. Misses the full early-stage growth. | Excellent — full investment benefits from early-stage gains. | Lump Sum |

| Volatile market (up and down unpredictably) | Excellent — Rupee Cost Averaging smooths the volatility. Buys more when low. | Risky — timing matters enormously. 2025 showed -20% to +14% dispersion. | SIP |

| Falling market (steady decline) | Good — keeps buying at lower prices. Each instalment cheaper than the last. | Poor — full investment depreciates from Day 1. | SIP |

| Sideways market (no clear trend) | Good — accumulates units at consistent prices. Compounding starts immediately. | Average — no gain or loss initially. Waiting is a hidden cost. | SIP |

| Post-crash recovery (market just bottomed) | Good — SIP misses a small part of the V-shaped rally. | Excellent — full investment benefits from the full recovery move. | Lump Sum at the bottom |

In 2026, India’s market environment is characterised by volatility — global tensions, geopolitical risk, FPI outflows, and policy uncertainty. In this specific environment, SIP’s volatility-smoothing advantage is at its most powerful. As the Whalesbook February 2026 analysis noted: “The projected economic growth for 2026, while strong for India, occurs amidst global uncertainties and potential trade headwinds, making precisely timing large inflows a speculative endeavor.”

4. The Master Comparison — SIP vs Lump Sum Across 10 Factors

This is the table to save. It covers every dimension that matters for a real investor making this decision.

| Factor | SIP | Lump Sum |

| Market timing risk | None — you invest at every NAV level | High — one wrong entry point can cost years |

| Emotional discipline required | Low — automatic monthly deduction removes emotions | High — watching a large investment fall 15% requires nerves |

| Rupee Cost Averaging | Yes — buy more units when market is low | No — single purchase price only |

| Compounding start date | Starts with first instalment | Starts on the single investment date |

| Ideal for | Salaried investors with regular monthly income | Bonus, inheritance, property sale, FD maturity proceeds |

| In a falling market | Benefit — cheaper units each month | Loss — full investment depreciates from Day 1 |

| In a strong bull run | Miss out on early gains if starting late | Full investment benefits from the entire rally |

| Tax management | Each instalment has its own holding period. Staggered LTCG over time. | Single holding period. Simpler but no annual LTCG exemption benefit. |

| Accessibility | Rs 500 minimum. Open to anyone. | Typically Rs 5,000 to Rs 10,000 or more needed to feel meaningful |

| Best suited for 2026 | Yes — volatile market benefits from averaging | Only if you have a large lump sum AND use STP (see Section 7) |

5. SIP Returns — Real Numbers Across Amounts and Time Horizons

The best argument for SIP is not theory — it is the numbers that ordinary Indian investors have actually earned.

How a Rs 5,000 Monthly SIP Grows Over Time (at 12% CAGR)

| Duration | Total Invested | Estimated Value | Extra Wealth Created | Multiplier |

| 5 years | Rs 3,00,000 | Rs 4,08,348 | Rs 1,08,348 | 1.36x |

| 10 years | Rs 6,00,000 | Rs 11,61,695 | Rs 5,61,695 | 1.94x |

| 15 years | Rs 9,00,000 | Rs 25,22,880 | Rs 16,22,880 | 2.80x |

| 20 years | Rs 12,00,000 | Rs 49,95,740 | Rs 37,95,740 | 4.16x |

| 25 years | Rs 15,00,000 | Rs 94,88,186 | Rs 79,88,186 | 6.33x |

| 30 years | Rs 18,00,000 | Rs 1,76,49,569 | Rs 1,58,49,569 | 9.80x |

In 2025 — How SIP Investors Fared vs Lump Sum Investors

| Metric | SIP Investors (2025) | Lump Sum Investors (2025) |

| Mutual fund schemes with positive returns | 97% of all schemes delivered positive SIP returns | Wide dispersion — range from -20% to +14% |

| XIRR range for SIP | Up to 37% in top performing schemes | Depended entirely on entry date in 2025 |

| Impact of market timing | None — spread over 12 monthly investments | Everything — investors who entered in Jan 2025 vs Nov 2025 had very different outcomes |

| Investor experience | Stable. Consistent. Predictable. | Highly variable. Some excellent. Many disappointing. |

6. Lump Sum — When It Actually Beats SIP

This article is not anti-lump sum. There are real, specific situations where investing a lump sum outperforms a SIP. Here they are.

| Situation | Why Lump Sum Wins | Example |

| You receive a large bonus or windfall during a market correction of 15%+ | Full investment immediately benefits from the recovery. No waiting. Maximum upside capture. | Investing Rs 10 lakh in April 2020 (COVID bottom) vs monthly SIP from Jan 2020 — lump sum at bottom wins significantly. |

| You have a confirmed short time horizon of 5 to 7 years | Less time for Rupee Cost Averaging to work its advantage. A single quality entry can match SIP over shorter periods. | Rs 5 lakh lump sum into a debt fund for a 3-year goal. SIP not necessary here. |

| Markets are clearly cheap — P/E ratios at historical lows | When valuations are statistically low, the probability of recovery is high. A lump sum at low P/E captures more of the subsequent rally. | March 2020 Nifty at 8,000 with P/E of ~18x (historical: 22x). Lump sum at that P/E crushed SIP returns. |

| You have very high financial knowledge and emotional discipline | Experienced investors who can actually wait for and deploy at market bottoms beat average SIP returns over long periods. | Alok Jain’s dip-buying strategy: Rs 3.9 crore vs Rs 3.38 crore for SIP over 30 years. Real but requires discipline most investors lack. |

The honest summary: lump sum beats SIP when you invest at the right time. The problem is that identifying the right time requires either remarkable timing skill or remarkable luck. In 2025, lump sum returns ranged from -20% to +14% depending purely on when in the year you invested. SIP investors had a 97% positive return rate. For most investors — especially those without deep market experience — SIP’s consistency outweighs lump sum’s theoretical upside.

7. STP: The Smarter Way to Invest a Lump Sum

Here is the solution that resolves the entire SIP vs lump sum dilemma for investors who have a large amount to invest: the Systematic Transfer Plan, or STP.

An STP works like this: you invest your entire lump sum in a liquid fund or ultra-short duration debt fund on Day 1. Then, every month, a fixed amount is automatically transferred from the debt fund into your chosen equity fund. You get the safety of parking the full amount immediately (earning 6 to 7% in the debt fund while waiting) and the market timing protection of spreading the equity investment over 6 to 12 months.

How STP Works — Priya’s Rs 5 Lakh Bonus Example

| Action | Without STP (Direct Lump Sum) | With STP (Smart Approach) |

| Day 1 | All Rs 5 lakh invested in equity fund at current NAV. | All Rs 5 lakh invested in Liquid Fund at 7% p.a. |

| Month 1 to 6 | Full Rs 5 lakh exposed to equity market volatility from Day 1. | Rs 83,333 per month transferred from Liquid Fund to Equity Fund. Remaining cash earns 7% while waiting. |

| If market falls 15% in Month 2 | Full Rs 5 lakh falls 15% = loss of Rs 75,000. | Only Rs 83,333 is in equity by Month 2. Remaining Rs 4.17 lakh is safe in liquid fund. Smaller exposure. |

| By Month 6 | All Rs 5 lakh has been in equity throughout. | All Rs 5 lakh deployed into equity through 6 averaging entry points. Liquid fund earned approximately Rs 17,500 in interim. |

| Long-term outcome | High if market goes up from Day 1. Painful if it falls first. | Consistent Rupee Cost Averaging. Less maximum regret. Better behavioural outcome. |

STP is the professional standard for deploying large one-time amounts in equity mutual funds. It combines the capital deployment speed of lump sum investing with the market timing protection of SIP. Most AMC websites and fintech platforms support STP setup in under 5 minutes once your liquid fund investment is in place.

The STP horizon should match your risk tolerance: 3 months if you have high conviction markets are cheap, 6 months for moderate uncertainty (current 2026 environment), 12 months if you are highly risk-averse or markets are at all-time highs.

8. Tax Differences Between SIP and Lump Sum

Taxation is one dimension where SIP and lump sum investing differ in ways that are not immediately obvious. Understanding this helps you plan redemptions efficiently.

How Each Method Is Taxed — Equity Funds (Finance Act 2024)

| Factor | SIP Tax Treatment | Lump Sum Tax Treatment |

| Holding period calculation | FIFO — each monthly instalment has its own purchase date and its own holding period. | Single investment date. One holding period for the entire amount. |

| LTCG eligibility | Units become LTCG-eligible (held 1+ year) on a rolling basis — Month 1 units after 13 months, Month 2 after 14 months, etc. | Entire investment becomes LTCG-eligible on a single date — exactly 1 year after investment. |

| Annual Rs 1.25L LTCG exemption | Can be used strategically each year as different batches of SIP units mature past 1 year. | All gains from redemption in one year — may exceed Rs 1.25L exemption in a single event. |

| Tax efficiency with annual redemptions | High — stagger SIP redemptions across years to maximise Rs 1.25L annual exemption. | Lower if lump sum is large and redeemed all at once above Rs 1.25L. |

| Complexity of tax calculation | Higher — each instalment is a separate purchase for tax purposes. | Lower — single purchase date, single cost basis. |

The practical tax advantage of SIP: for large equity fund holdings, a long-running SIP allows you to harvest gains gradually each year — redeeming units that have crossed 1 year while keeping the rest invested. If managed carefully, each year’s redemption can stay within the Rs 1.25 lakh LTCG exemption, resulting in zero tax on a significant portion of your gains over time. A financial advisor or Chartered Accountant can help you plan this optimally.

9. The Decision Framework — Which One Is Right for You?

After all the data, here is a simple, practical framework to make the decision for your specific situation.

| Your Situation | Right Choice | Why |

| You earn a monthly salary and want to invest regularly | SIP — always | Monthly income matches monthly investment. No timing. No discipline needed. Set up NACH and forget. |

| You received a bonus, gratuity, or maturity amount (under Rs 5 lakh) | STP over 3 to 6 months | Too small for complex planning. STP gives you market timing protection without overthinking. |

| You received a large windfall (above Rs 5 lakh — property sale, retirement benefit, inheritance) | STP over 6 to 12 months into equity + keep 20-30% in liquid/debt fund | Large amounts require more care. STP over 6 months in volatile 2026 market is prudent. |

| Markets just corrected 15 to 20% from recent highs | Lump sum is acceptable — consider investing 50% now, 50% via STP over 3 months | Correction creates a margin of safety. But never invest 100% at once even in corrections. |

| You are a first-time investor with limited savings | SIP — Rs 500 to Rs 2,000 per month to start | Small amounts make lump sum impractical. SIP builds the habit before building the corpus. |

| You have high investment knowledge and track market cycles actively | Hybrid: ongoing SIP for discipline + lump sum on confirmed 10%+ corrections | This is Alok Jain’s dip-buying strategy. Works if you have the knowledge and discipline to wait. |

| You are near retirement (5 to 10 years away) | Continue SIP but shift allocation toward BAF or debt. Use STP for any lump sums. | Goal proximity reduces time for SIP averaging to work. Capital protection becomes priority. |

10. Frequently Asked Questions

Q1: Which is better — SIP or lump sum in mutual funds?

For most Indian retail investors, SIP is the better approach because it removes market timing risk, enables Rupee Cost Averaging, requires only Rs 500 per month, and builds the discipline of regular investing. A 30-year Nifty study by Alok Jain of Weekend Investing found that a pure monthly SIP and a dip-buying lump sum strategy with the same total investment delivered similar final values (Rs 3.38 crore vs Rs 3.90 crore) — the difference being execution difficulty, not returns. For investors with a lump sum, a Systematic Transfer Plan (STP) is the best of both worlds.

Q2: Can lump sum mutual fund investment beat SIP?

Yes — in specific conditions. Lump sum beats SIP when the entire amount is invested at or near a market bottom, when markets enter a sustained bull run immediately after investment, or when the investor is disciplined enough to wait and deploy only during 10%+ corrections. In 2025, the best-timed lump sum investments returned up to 37%+ while the worst-timed ones returned -20%. SIP investors in 2025 saw 97% of schemes deliver positive returns. The potential upside of lump sum is real but requires timing accuracy that most investors cannot consistently achieve.

Q3: What is STP and why is it better than direct lump sum investing?

STP stands for Systematic Transfer Plan. It involves investing your entire lump sum in a liquid or debt fund first, then automatically transferring a fixed amount monthly into your chosen equity fund. This gives you two advantages: your lump sum earns 6 to 7% in the debt fund while waiting (rather than sitting in a savings account), and your equity investment is spread over 6 to 12 months to reduce timing risk. STP is the standard professional approach for deploying large one-time amounts in equity mutual funds. Most AMC platforms and fintech apps support STP setup in minutes.

Q4: Is SIP or lump sum better for tax saving?

For tax savings under Section 80C, both SIP and lump sum investments in ELSS funds qualify for the same Rs 1.5 lakh annual deduction. However, in a SIP, each monthly instalment has its own 3-year lock-in from its investment date. A lump sum ELSS investment unlocks the entire amount on a single date — simpler to manage. For LTCG tax planning at redemption, SIP allows you to stagger withdrawals across financial years to maximise the Rs 1.25 lakh annual LTCG exemption. A CA can help you optimise both approaches for your specific tax situation.

Q5: Should I do SIP or lump sum if I have Rs 1 lakh to invest right now?

For Rs 1 lakh in the current 2026 market environment — with global volatility, geopolitical risk, and elevated uncertainty — an STP of Rs 1 lakh over 3 to 4 months into a quality equity mutual fund is the most sensible approach. Park the full Rs 1 lakh in a liquid fund today (earning approximately 7% p.a.), and set up a monthly transfer of Rs 25,000 to Rs 33,333 into your equity fund. This gives you market entry at 3 to 4 different price points, reduces your maximum regret if markets fall further, and still gets your full investment deployed within a quarter.

Conclusion

The SIP vs lump sum debate does not have a single correct answer. It has a correct answer for each investor based on their income pattern, the size of their investment, their risk tolerance, and the current market environment.

For most Indian retail investors with monthly salaries, SIP is the right default. It is automatic, accessible from Rs 500, requires zero market knowledge, and has delivered consistent wealth creation across 30 years of Nifty data. In 2025, 97% of mutual fund schemes delivered positive returns for SIP investors. That number says everything.

For investors with lump sums — from bonuses, inheritances, or maturing investments — STP is the professional-grade bridge between lump sum’s potential upside and SIP’s timing protection. Park the full amount in a liquid fund. Transfer monthly into equity. Benefit from both.

The 30-year data’s deepest insight is not about SIP vs lump sum at all. It is this: the investor who stays invested through market cycles — whether via SIP, lump sum, or STP — always ends up ahead of the investor who waits for the perfect moment that never quite arrives. Consistency beats timing. Every time.

Continue reading: This article is part of our Mutual Funds India 2026 content hub at aspirixwriters.com/mutual-funds/

Complete Guide to Mutual Funds India 2026

Author

CA Ajay Khandelwal is a Chartered Accountant and financial expert with over 21 years of experience in taxation, compliance, and business advisory. As a key expert at AspirixWriters, he provides practical insights on income tax, financial planning, and regulatory matters, helping readers make informed financial decisions.

Author profile CA. Ajay Khandelwal

Disclaimer

This article is for educational and informational purposes only. It does not constitute personal financial advice, investment advice, or a recommendation to follow any specific investment strategy.

Mutual fund investments are subject to market risks. All return figures cited are historical and illustrative — actual results will vary. The 30-year Nifty study cited is based on Alok Jain’s analysis published in BusinessToday (January 2, 2026) and is presented for educational purposes. Tax treatment discussed is based on current law as of March 2026 and subject to change. Please consult a SEBI-registered Investment Advisor and a Chartered Accountant before making investment decisions.

Find a SEBI-registered investment advisor at: sebi.gov.in

References

[1] India Tax Tools — SIP vs Lump Sum Investment in 2026: Which Gives Better Returns? | STP explained | FIFO tax treatment | Decision flowchart | 3 weeks ago — https://indiataxtools.com/blog/sip-vs-lump-sum-investment-in-2026-which-gives-better-returns/

[2] NSE India — Nifty 50 historical P/E ratio data | Market valuation benchmarks | nseindia.com — https://nseindia.com/products-services/indices-nifty50-index

[3] ICICI Bank — SIP vs Lump Sum: Which Is Better in 2026? | Risk-averse vs risk-tolerant framework | Market opportunity deployment — https://www.icici.bank.in/personal-banking/blogs/investments/mutual-funds/sip-vs-lump-sum

How to Check Is Your AI System High-Risk Under the EU AI Act (2026)

Is Your AI System High-Risk Under the EU AI Act (2026)? Rohan is a product…

My Startup Uses ChatGPT. Do I Really Need an AI Policy? (2026 Guide)

Startup Chatgpt AI Policy Arjun runs a 12-person fintech startup in Mumbai. His team uses…

Someone Posted My Photos Online Without Permission. What Can I Do?

Image misuse online The Moment You Realise It’s Happened You’re scrolling through your phone, and…

My SIP Is in Loss. Should I Stop Investing?

SIP in loss – Riya is a 28-year-old software engineer in Bengaluru. She started a…

Does the EU AI Act Apply to Indian Companies? A Complete Compliance Guide (2026)

Does the EU AI Act Apply to Indian Companies? 1. The Scenario A Bengaluru-based HR-tech…

AI SEO Checklist 2026: How to Rank Your Website in ChatGPT, Perplexity & Google AI Overviews

Here is an uncomfortable reality:Read expert guide on AI SEO Checklist, Research by Dr. Rekha…