Riya is a 28-year-old software engineer in Bengaluru. She started a ₹5,000 SIP two years ago, feeling proud about finally investing. Then the market fell sharply. Today her app shows a big red number: –18%.

Her WhatsApp group is buzzing. Friends are saying “stop your SIP,” “wait for markets to recover,” “it’s going to get worse.” Her colleague already stopped his. Her mother is worried she’s “losing money every month.”

Riya is about to do the one thing that would genuinely hurt her long-term wealth — stop her SIP at exactly the wrong time.

How SIP Works: A Simple Guide with SIP Calculator Monthly for 2026

Quick Answer

When your SIP shows a loss during a market fall, it usually means your investments have dropped temporarily in value — not that you have permanently lost money. SIPs are built to handle market falls by buying more units at lower prices, which reduces your average cost over time. In most cases, for goals that are 7 or more years away, continuing your SIP is the right call. Stopping during a fall usually does more harm than the market ever did.

Overview

- A red number on your SIP screen is a temporary paper loss, not a permanent destruction of your money.

- SIPs buy more units when prices are lower — that is the whole point. A falling market is doing you a favour, not a disservice.

- Stopping your SIP during a fall locks in a higher average cost and means you miss the recovery — both at once.

- The longer you stay invested, the lower your chance of ending up with a loss. Data shows the odds of losing money in a well-chosen equity SIP over 7+ years are very low (AMFI investor education).

- Not all stops are wrong. If your goal is less than 3 years away, or your emergency fund is empty, or you’re in the wrong fund — those are worth reviewing. The market crash isn’t the issue; the fit is.

Does This Apply to You?

| Reader | Should you keep reading? |

|---|---|

| Salaried employee with SIP | Yes — you need a clear decision framework, not just reassurance |

| First-time investor | Yes — understanding this early saves years of expensive mistakes |

| Parent investing for a child’s education | Yes — long-term goals are exactly where this matters most |

| Freelancer or self-employed | Yes — your situation has one extra layer around income stability |

| Senior citizen | Yes — but with a different conclusion; equity SIP may not suit your timeline |

| Student or young professional starting out | Yes — this is the best time to build the right habits |

| Anyone who stopped their SIP last month | Especially yes |

Why This Matters

Your future money is at stake — not just this month’s returns.

A SIP is not a savings account. It is a long-term wealth-building tool, and its power comes from staying in it through the difficult periods, not just the easy ones. The single biggest threat to a SIP’s performance is not a market crash — it is the investor’s own decision to stop during that crash (indiatoday.in, stock market crash SIP article 2026).

The numbers are real.

AMFI — the body that governs India’s mutual fund industry — reports that SIP inflows in India remained strong and even reached record levels during recent periods of high market volatility. Millions of Indian investors continued their SIPs despite seeing red numbers, and history shows the majority of them were right to do so (AMFI, monthly SIP data).

The cost of stopping is invisible but huge.

If you stop your SIP during a 20% market fall, you miss the cheapest units you will ever buy in that cycle. When the market recovers — and historically, it always has — those cheap units are the ones that drive the biggest gains. The investor who paused and restarted “when things looked better” almost always re-entered at higher prices, bought fewer units, and ended up with a smaller corpus than the investor who simply stayed.

Practical Insight: The pain of watching your SIP show a loss is emotional and real. But the cost of stopping is financial and permanent. These two things are not the same.

Understanding the Problem

Why does a SIP show losses at all?

A SIP invests a fixed amount in a mutual fund every month. That fund holds stocks or bonds. When markets fall, the price of those stocks drops, so the value of your units drops. Your screen shows a negative return. But — and this is the crucial part — you still hold the same number of units. You haven’t sold anything. The loss is only real if you sell.

Why do people panic?

Three psychological forces push investors toward stopping at exactly the wrong time:

Loss aversion. Humans feel the pain of a loss about twice as strongly as the pleasure of an equivalent gain. Seeing ₹1,00,000 become ₹82,000 on screen feels worse than it actually is in financial terms — and it pushes people toward action even when inaction is better (SEBI investor education, behavioural finance content).

Recency bias. When markets have been falling for weeks, our brain tells us they will keep falling. We project recent experience into the future and forget that markets have recovered from every single major crash in Indian history.

Herd behaviour. WhatsApp groups, news headlines, and social media amplify fear. When people around us are stopping their SIPs, it feels reckless to continue. This is herd behaviour — and it is one of the most reliable ways to destroy long-term wealth.

The three most common misconceptions:

“I’m throwing good money after bad.” — No. You are buying discounted units of the same assets. This is the opposite of throwing money away.

“I’ll restart when things stabilise.” — By the time things “look stable,” the recovery has already happened. You’ve paid higher prices for fewer units.

“The market might keep falling, so I should wait.” — Nobody knows when markets will bottom out. Not you, not your broker, not a financial advisor on television.

What Actually Happens to SIP When Markets Fall

This is where most people’s understanding breaks down — and where the real power of SIPs lives.

Rupee cost averaging in plain English:

When you invest a fixed amount every month, you automatically buy more units when prices are low and fewer units when prices are high. You don’t have to think about it. It happens by design.

Here is a simple example:

| Month | Market Condition | NAV (₹) | SIP Amount (₹) | Units Bought |

|---|---|---|---|---|

| January | Normal | 100 | 5,000 | 50.0 |

| February | Market falls 20% | 80 | 5,000 | 62.5 |

| March | Market falls further | 70 | 5,000 | 71.4 |

| April | Market recovers to 90 | 90 | 5,000 | 55.6 |

| May | Market back to 100 | 100 | 5,000 | 50.0 |

Total invested: ₹25,000 · Total units: 289.5 · Value at ₹100: ₹28,950 · Gain: ₹3,950

An investor who stopped in February missed the cheapest months entirely. Their average cost per unit is higher, and their final corpus is smaller — even though the market ended at the same place.

SIP vs lump sum during a crash:

A lump-sum investor who invested ₹25,000 in January and watched the market fall to ₹70 is sitting on a larger temporary loss and has no mechanism to average down. The SIP investor’s averaging does that work automatically, month by month (news.abplive.com, SIP during market fall explainer).

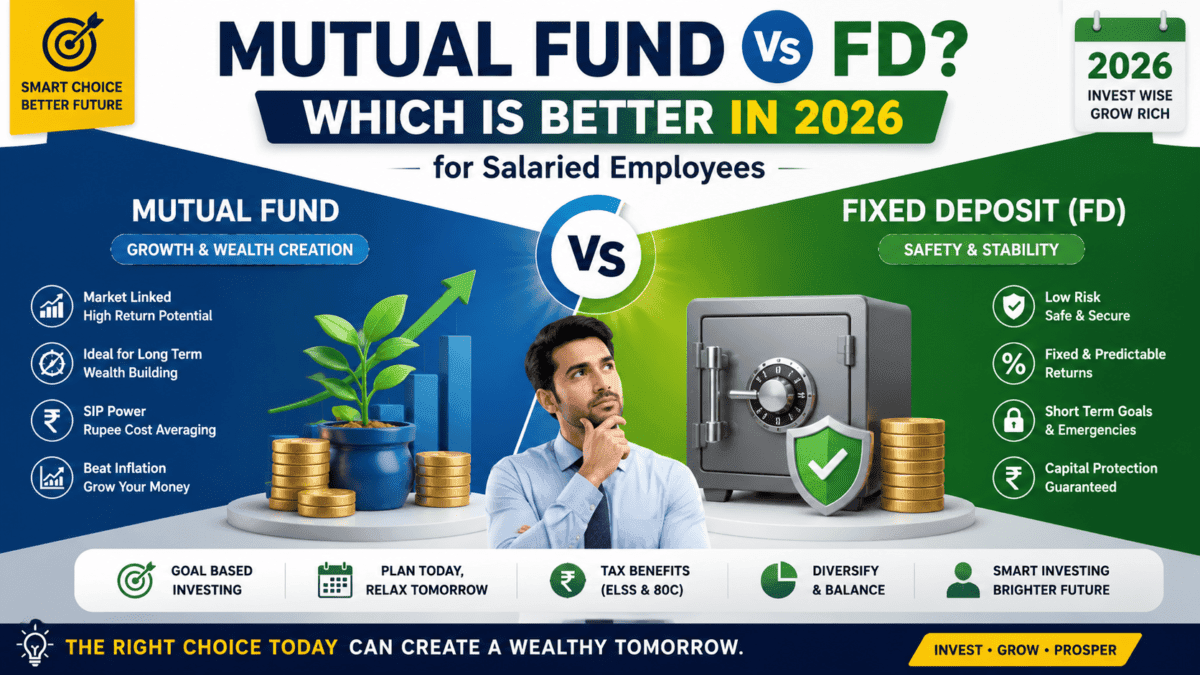

SIP vs Lump Sum 2026: Which Is Better?

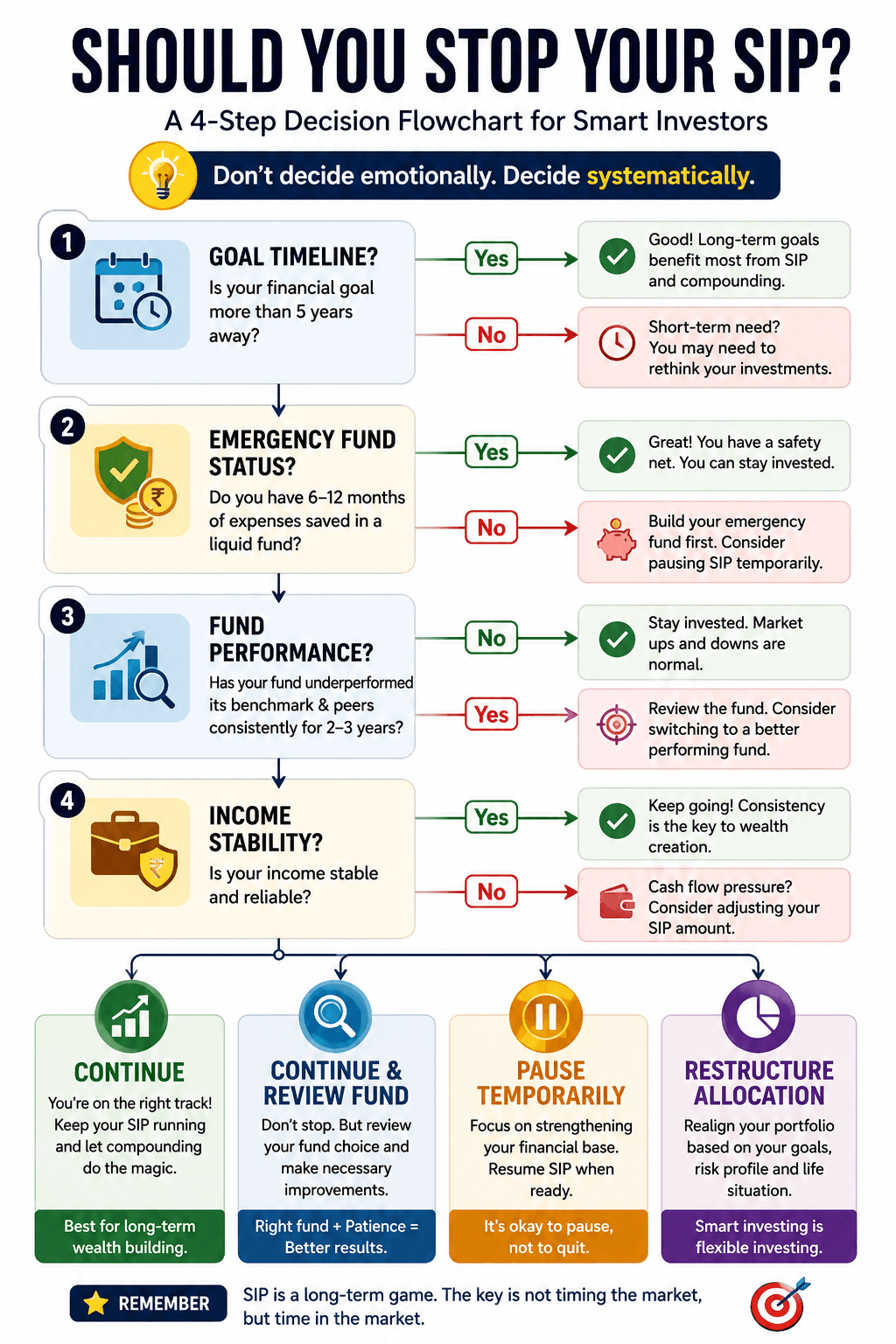

Should You Stop, Continue, or Increase Your SIP?

Use this decision framework. Work through each question in order.

Question 1: When do you need this money?

- More than 7 years away → Continue your SIP. This is exactly what SIPs are designed for. Short-term volatility is normal and expected.

- 5 to 7 years away → Continue, but review your fund type. Ensure you’re not in a high-risk small-cap fund if your timeline is closer to 5 years.

- 3 to 5 years away → Think carefully. Equity SIPs can deliver but carry meaningful risk at this horizon. Consider shifting toward a more balanced approach gradually.

- Less than 3 years away → Equity SIP was probably not the right choice for this goal. This is a product suitability issue, not a market timing issue. Speak to a financial advisor about moving to debt funds or fixed-income options.

Question 2: Is your emergency fund in place?

- Yes, you have 3–6 months of expenses in a liquid fund or savings account → Continue your SIP. You can absorb short-term cash shocks without touching your investments.

- No, your emergency fund is missing or too small → Build it first. Increasing your SIP right now, before your safety net is ready, is the wrong order of operations (SEBI investor education, emergency fund guidance).

Question 3: Is the fund itself the problem?

Not all SIP losses are just market-related. Sometimes the fund has genuinely underperformed its benchmark or category peers consistently over 3+ years. Check:

- Is the fund’s performance worse than similar funds in the same category?

- Has the fund manager or strategy changed recently?

If yes to either — this is worth reviewing with your advisor. The answer may be to switch funds, not stop investing entirely.

Question 4: Can you afford to continue?

If your income has genuinely dropped — job loss, medical emergency, business disruption — it is perfectly acceptable to pause your SIP temporarily. Pausing is not the same as stopping. You keep your existing units. You stay invested. You simply don’t add new money for a few months. Most mutual funds allow this with no charges (AMFI, SIP operational guidelines).

Practical Insight: “Should I stop my SIP?” is almost always the wrong question. The right questions are: Is my goal timeline correct? Is my fund right for me? Is my financial foundation stable? Answer those and the SIP decision usually answers itself.

How Long Does It Take to Recover?

This is the question most people really want answered — and the answer is more reassuring than most people expect.

| SIP Holding Period | Historical Probability of Positive Returns |

|---|---|

| 1 year | Around 65–70% — meaningful risk of negative returns |

| 3 years | Around 75–80% — better, but still not reliable |

| 5 years | Around 90–95% — strongly favourable for most market conditions |

| 7+ years | Historically above 99% for broad index-based equity SIPs |

| 10+ years | Very close to 100% for diversified equity funds |

(Based on long-term Nifty 50 and large-cap fund analysis widely cited by AMFI and financial research firms including ET Money. Past performance does not guarantee future results.)

The key message here is simple: time is the most powerful variable in a SIP. A SIP that looks terrible after 2 years often looks excellent after 7. The loss on your screen right now is most likely a chapter in a longer story, not the ending.

Real-Life Examples

Example 1: The investor who stopped vs the investor who continued

Imagine two colleagues, Arjun and Deepa, both starting a ₹10,000 monthly SIP in a large-cap equity fund in 2019. The COVID-19 crash of March 2020 hits. Markets fall nearly 38%.

Arjun panics and stops his SIP in April 2020. He restarts it in October 2020 when “things look better” — by which point the market has already recovered 40% from its bottom.

Deepa does nothing. She keeps her ₹10,000 going every month through the crash.

By December 2021, Deepa’s portfolio is significantly larger than Arjun’s — not because she was smarter about market timing, but because she bought the cheapest units in the entire cycle while Arjun sat on the sidelines (indiatoday.in, SIP crash recovery examples 2026).

Example 2: The investor in the wrong product

Meena is 58 and started a ₹15,000 monthly SIP in a small-cap fund three years ago for a goal she needs in 18 months. The market falls and she sees –28%. She blames the market.

But Meena’s problem isn’t the market. It’s that she was in a high-volatility product for a near-term goal. This is a product suitability issue. The right answer for Meena is not “continue or stop” — it is to work with an advisor to move to a more appropriate product now, absorb the current loss, and not repeat the mistake.

Did You Know? AMFI reported that India’s total SIP inflows remained above ₹25,000 crore per month even during periods of significant market correction in 2025–26 — suggesting that the majority of experienced SIP investors chose to continue regardless of short-term losses (AMFI, monthly SIP data releases).

Common Mistakes

- Stopping the SIP during the biggest fall — this is precisely when units are cheapest. Stopping here is the worst possible timing.

- Redeeming existing units along with stopping the SIP — now you have turned a paper loss into a real, permanent loss.

- Confusing a fund’s short-term underperformance with a market problem — sometimes the fund is the issue, not the market.

- Restarting SIP only after markets have recovered — you re-enter at higher prices and miss the entire recovery rally.

- Ignoring the emergency fund and stopping SIP to build one — you should have the emergency fund before or alongside the SIP, not instead of it.

Myth vs Fact

| Myth | Fact |

|---|---|

| “My SIP is losing money permanently.” | You hold units. A falling NAV is a temporary paper loss unless you sell (SEBI investor education). |

| “I should wait for markets to recover before restarting.” | The recovery is what you need to be invested through — not the calm after it (indiatoday.in, stop SIP in panic 2026). |

| “Stopping SIP protects me from further losses.” | Stopping stops new purchases. Your existing units still move with the market. And you miss the cheap units during the fall. |

| “SIP guarantees profit.” | No investment guarantees profit. SIPs reduce risk through averaging and time — they do not eliminate it (AMFI, mutual fund risk disclosure). |

| “If my SIP is negative after 3 years, it has failed.” | Three years is too short to judge an equity SIP. Most losses resolve meaningfully by year 5–7. |

Practical Checklist

Before you stop your SIP, check every item on this list:

- [ ] Is my financial goal more than 5 years away?

- [ ] Do I have 3–6 months of expenses in a liquid emergency fund?

- [ ] Is this fund underperforming its category peers consistently, or just the market generally?

- [ ] Have I had this SIP running for at least 3 years?

- [ ] Am I stopping because of data, or because of fear and social pressure?

- [ ] Do I understand that stopping means missing the cheapest units in this cycle?

- [ ] Have I spoken to a financial advisor before making this call?

If you answered “yes” to the first two and “no” to the last one — the evidence strongly suggests you should continue your SIP.

During a market fall — do’s and don’ts:

| Do | Don’t |

|---|---|

| Keep your SIP running | Stop because your WhatsApp group told you to |

| Review your asset allocation if needed | Redeem long-term investments for short-term comfort |

| Build or top up your emergency fund | Start a new aggressive SIP without a safety net |

| Check if your fund suits your timeline | Switch funds based on 6-month returns |

| Stay patient and review annually | Check your portfolio value every day |

Exit load:

Many equity mutual funds charge an exit load — typically 1% — if you redeem within 1 year of purchase. For a SIP running for 2 years, the last 12 months of units may still attract exit load. This is money paid directly out of your corpus with no benefit to you (SEBI, mutual fund exit load regulations).

The real cost of stopping and restarting:

Stopping doesn’t cost you a fee. But restarting when markets recover means you buy the same units at a higher price. That price difference — the gap between the cheapest point during the crash and the “safer” price when you came back — is the actual cost of pausing. It doesn’t show up as a charge. It shows up as a smaller final corpus.

Practical Insight: Stopping and restarting a SIP has no formal fee. But it has a very real economic cost — you miss the recovery rally that follows every crash, and you buy back in at higher prices. This invisible cost is often larger than any market loss you were trying to avoid.

must explore – Income Tax India 2026 : A Complete Guide

Frequently Asked Questions

1. Can I lose money in a SIP?

Yes, in the short term. Equity SIPs carry market risk, and short-term losses are normal and expected. However, historical data shows the probability of loss reduces dramatically over longer holding periods — approaching near-zero for well-diversified equity SIPs held for 7 or more years (AMFI, long-term SIP data).

2. What should I do if my SIP is showing negative returns?

First, check your goal timeline. If you have 5+ years to go, the most evidence-backed action is to continue. If you’re in the wrong type of fund for your timeline, speak to an advisor about switching — not stopping.

3. Is SIP safe during a market crash?

Safe is the wrong word for equity investments. SIPs are designed to work through market crashes by averaging your purchase cost downward. They don’t prevent crashes — they use crashes to your advantage if you stay invested (SEBI investor education on mutual funds).

4. Can I pause my SIP temporarily?

Yes. Most mutual fund houses allow you to pause SIP instalments for 1–6 months without cancelling the SIP entirely. You keep your existing units. This is a reasonable option if you’ve had a genuine income shock. It is not a strategy for avoiding market volatility.

5. Should I increase my SIP during a market crash?

Only if you have your emergency fund fully in place, your income is stable, and you have room in your monthly budget. If those conditions are met, a market fall can be an excellent time to top up — you are buying more units at lower prices. If those conditions are not met, protect your foundation first.

6. Is SIP better than lump sum during a crash?

For most individual investors, yes. A lump sum makes one big purchase at one price — which could be before further falls. A SIP spreads purchases across multiple months, averaging the cost automatically. During a crash, this is a genuine structural advantage.

7. How long should I continue my SIP?

Until your goal is 1–2 years away, at which point you should start gradually shifting to less volatile assets to protect what you’ve built. For most long-term goals — retirement, children’s education, home purchase — this means staying invested for 10–20 years.

8. What happens if I stop my SIP but don’t redeem?

Your existing units stay invested and continue to move with the market. You simply stop adding new units. This is better than redeeming, but you still miss the low-cost units available during the fall. And human nature means many investors who “just stop” end up redeeming a few months later too.

What Should You Do Next?

Salaried employee / young professional: Keep your SIP running. Add one task to your calendar: annual review of your fund’s performance against its category peers. That’s the only review your SIP needs — not a monthly panic check.

First-time investor: If you are less than 3 years into your SIP journey, you are in the phase where losses are most visible and least meaningful to your final outcome. Stay patient and read your fund’s scheme information document so you understand what you’re in.

Parent saving for education: Check your goal date. If the degree starts in less than 4 years, it’s time to gradually shift a portion toward debt funds — not because of this crash, but because the timeline now calls for it.

Freelancer or self-employed: Your priority right now is your emergency fund — 6 months of expenses minimum, not 3. Once that’s solid, your SIP decision is easier. If you have to choose between building the emergency fund and continuing the SIP, build the fund first.

Senior citizen: Equity SIP may not be appropriate for goals within 3–5 years. Speak to a financial advisor before making any changes — the answer here is genuinely individual and depends on your overall portfolio, income, and needs.

Anyone who already stopped: You haven’t permanently lost anything yet. The question now is whether to restart. If your goal is still 5+ years away and your emergency fund is in place, restarting — even at today’s prices — is almost certainly better than waiting for the “right moment” that never quite arrives.

must explore –Mutual Funds India 2026: Complete Beginner’s Guide

Conclusion

The red number on your SIP screen is not a signal to stop. It is a signal that the market is doing exactly what markets do — moving through a cycle. SIPs were designed for exactly this moment: to keep buying through the fall so that when the recovery comes, you hold more units at a lower average cost than any investor who waited on the sidelines.

The investors who build wealth through SIPs are not the smartest stock-pickers or the best market timers. They are the ones who understood one simple principle: time in the market beats timing the market — and they stayed in.

Don’t let a temporary paper loss make a permanent dent in your future.

Author –

CA Ajay Khandelwal is a Chartered Accountant and financial expert with over 21 years of experience in taxation, compliance, and business advisory. As a key expert at AspirixWriters, he provides practical insights on income tax, financial planning, and regulatory matters, helping readers make informed financial decisions.

Author Profile CA. Ajay Khandelwal

Review Information

Last Reviewed: June 2026 Next Review: Within 6 months or on any major regulatory change to mutual fund rules or capital gains tax provisions.

Disclaimer

This article is for educational and informational purposes only. It does not constitute personal financial advice, investment advice, or a recommendation to follow any specific investment strategy.

explore –

- Academic Writing

- AI in Business & Marketing

- AI in Content Creation

- AI in Research

- AI in Research & Education

- AI In SEO

- AI Regulatory Framework

- AI Tools & Review

- Finance

- Indian Laws

- Legal Drafting & Pleading

- Trending

- Writing & Content Creation

My SIP Is in Loss. Should I Stop Investing?

Riya is a 28-year-old software engineer in Bengaluru. She started a ₹5,000 SIP two years…

Mutual Fund Vs FD? Which Is Better In 2026 for Salaried Employees

One Gives Stability. The Other Builds Long-Term Wealth. Most Salaried Employees Need Both. If you…

Mutual Funds India Complete Beginner’s Guide 2026

Mutual Funds India 2026 Complete Beginner’s Guide to Benefits, SIP, Types & SEBI New Rules…